{kind=link}

Auto-Enrolment Into Pensions: An Option For Ireland?

5 Mar 2014Introduction1

For most individuals in most countries starting a pension requires taking an active decision to do so. Over the past number of years schemes at both corporate and national level have changed this fact. Under these schemes (described as auto-enrolment schemes), if an employee does nothing, a portion of their pay will automatically be directed into a pension fund. The saving is not forced – the employee can opt out and choose not to do any pension saving – but to do so requires them to take an active decision. Changing the default option has been shown (and the evidence for this is discussed below) to dramatically increase rates of enrolment in pensions.

Such a scheme has been recently been introduced nationally in the UK and a national scheme in New Zealand has some features of auto-enrolment.

A national system of auto-enrolment can be considered a middle ground between a system in which saving into a private pension is compulsory (as it is in Australia and several Latin American countries) and a system such as that which exists in most countries (including Ireland) where private pension saving is purely voluntary. The advantages of compulsion for increasing pensions saving are clear – an automatic and immediate increase in pension saving and a reduction in the proportion of those currently of working age who will have inadequate resources in retirement. The disadvantages are just as clear – the removal of individual freedom and perhaps political difficulties in implementation. These issues are not explored further here, though they do deserve serious consideration.

The proposition that auto-enrolment will increase rates of enrolment in pensions comes from the premise that there are many individuals who have made a decision to start a pension but who have yet to put their plans into effect – that is, who are simply procrastinating. If such individuals are auto-enrolled into a pension fund it is likely that they will not opt-out – and further, given that they have made (but not enacted) the decision to increase their saving, it is likely that they will be content to have been given that push to save. This type of behaviour has been formalised in economic models and is described as behaviour that is “time-inconsistent”2.

I emphasise below that auto-enrolment has many attractive features. However, this commentary does not argue unambiguously for its introduction in Ireland. Such a recommendation would require first – a comprehensive analysis (that takes into account likely state pension income) of the extent to which there is an under-saving problem in Ireland and if so among whom and second – an investigation of the alternatives to auto-enrolment – in particular compulsory pension saving.

This commentary is organised as follows. Section 1 summarises the national scheme that is now in place in the UK. This gives a sense of what a national scheme might (though not necessarily should) look like. Section 2 summarises the evidence on what effect introducing auto-enrolment in pensions can have on pension participation rates and on rates of contribution. Section 3 considers a number of design issues that would need to considered should the Irish Government decide to introduce a similar scheme. Section 4 concludes.

1 Auto-enrolment in the UK

A national auto-enrolment scheme was rolled out in the UK in October 2012. Key features are outlined below3. All pound sterling figures are converted to euro figures at an exchange rate of €1 = £0.82 – the approximate exchange rate on 30 Jan 2014. To give context to the earnings figures outlined note that employment at 40 hours a week at the UK minimum wage would yield an income of £13,100/€16,000, while median earnings for someone working between 35 hours and 60 hours in 2011 were £25,400/€30,100.

- All employees between the ages of 16 and 74 must be offered a ‘workplace pension scheme’.

- Those between the ages of 22 and the State Pension Age (currently 62 and rising for women, 65 and planned to rise for men) and earning over a certain amount (currently £9,440/€11,500 per year) must be automatically enrolled into the pension scheme.

- Those between 16 and 21, those over the State Pension Age and under 74 and those with earnings under £9,440/€11,500 can join a workplace pension scheme if they wish. Their employer is obliged to offer one if the employee asks. However, these individuals are not automatically enrolled.

- Employees can, after being enrolled, opt-out of the scheme by filling in a form (available from the pension provider) and returning it to their employer. However, employers are obliged to re-enrol these employees every three years, at which point the employee must actively opt-out again if he/she wishes not to remain in the scheme.

- The minimum amount that must be paid into the scheme by employers will be 3% of gross earnings between £5,668/€6,900 and £41,450/€50,500 when the scheme is fully in place (2018). The minimum contributions are being phased in so that the current minimum is less.

- The minimum amount that must be paid into the scheme by employees will be 4% of gross earnings between £5,668/€6,900 and £41,450/€50,500 in 2018. This minimum employee contribution is also being phased in and is currently less.

- Tax relief is added to the employee contributions. Though there are some important differences which I don’t discuss here, the taxation of pensions in the UK takes a broadly similar form to that in Ireland. Contributions to pension funds in the UK are made out of gross income (that is there is tax relief at the employee’s marginal rate). Funds subject to a lifetime contribution maximum of £1.5m/€1.8m and an annual contribution maximum of the lesser of earnings and £50,000/€61,000 although these quantities are scheduled to fall somewhat in the coming years. 25% of DC funds can be taken after the age of 55 in a tax-free lump sum. The remainder must be converted into a (taxable) annuity.

By 2018, all employers will be obliged to comply with the above set of rules. The largest employers must already be in compliance while smaller employers are being given more time.

The UK is not the first country to introduce a national auto-enrolment programme for pension saving. KiwiSaver is a scheme in the New Zealand that contains many similar features which was established in 2007. A key difference is that employees are only defaulted into KiwiSaver when they start a new job. The current New Zealand government has stated that it plans to extend auto-enrolment to those not changing jobs when it feels it can meet the associated cost. A comparison between KiwiSaver and the UK system can be found in Pensions Policy Institute (2012).

The UK government has established the National Employment Savings Trust (NEST), a non-profit organisation, accountable to Parliament but independent of government to receive and manage employee funds (though employers are free to use other, new or existing, providers, should they wish to do so). The annual management charge is 0.3% (low compared to prevailing charges in both Ireland and the UK), and contributions are subject to a one-time charge of 1.8% on entry to the fund. NEST state that they anticipate removing the charge on contributions once the costs of establishing the scheme are met.

2 Evidence on auto-enrolment and pension saving?

In this section, I review two pieces of evidence that show that a policy of automatic enrolment can increase the proportion of people saving in a pension.

Evidence from a firm in the US

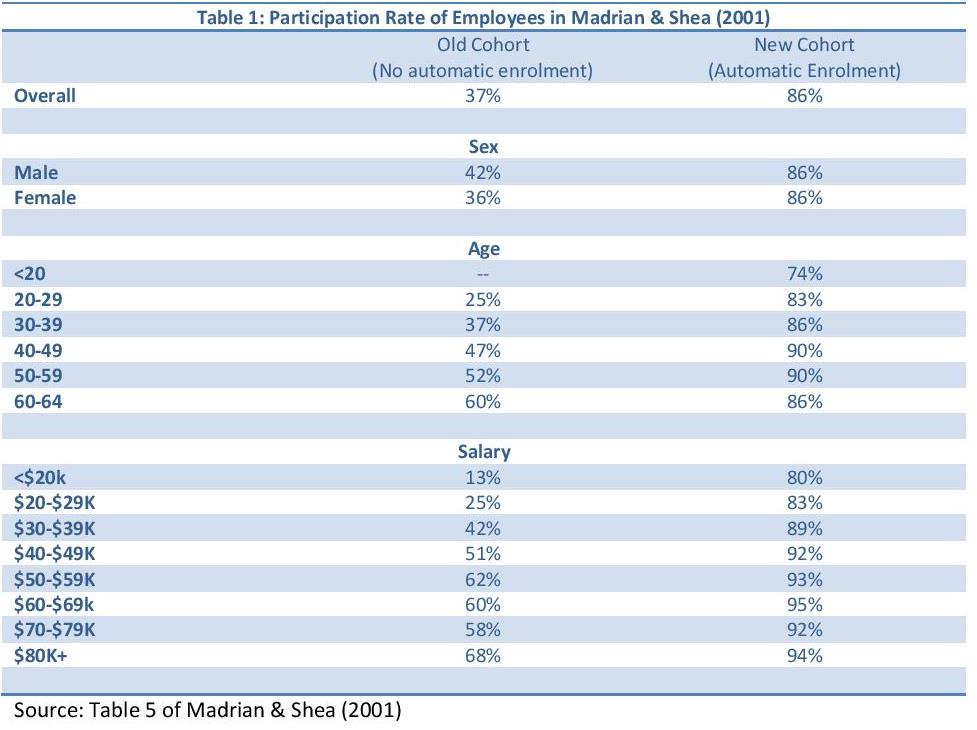

Madrian & Shea (2001) looked at the behaviour of two cohorts of employees of the same (unnamed in their paper) US Fortune 500 firm. In 1998, the firm changed its policy regarding employee participation in a 401k pension plan (similar to a Defined Contribution plan). Prior to that year, an employee had to fill out a form to authorise their employer to deduct a pension contribution from their salary, they had to chose a contribution rate, and they had chose how they would like their pension pot to be invested. Under the revised rules, new employees were defaulted in unless they informed their employer that they would like to opt out. Table 1 shows the difference between the proportion of the old cohort (who had to opt in) and the new cohort (who had to opt out).

The differences between the two sets of participation rates is striking and are seen across all income and age groups. The most striking results are found at younger ages and lower incomes – the groups among which we might be most concerned about under-saving.

Madrian & Shea also draw attention to the effect of auto-enrolment on the rate of contribution chosen by employees. In the firm in question, the default option was a 3% contribution. Unsurprisingly, most of those who participated in the auto-enrolment scheme but who would not have participated in the opt-in scheme chose the default contribution level. More interestingly, the authors present evidence suggesting that some of those who would have opted in at a rate different from 3% under the opt-in scheme choose 3% in the auto-enrolment scheme. The default level of contribution seems to have some persuasive power even for those who would have signed up for the scheme in the absence of auto-enrolment. This fact suggests some care need be taken in choosing the default rate of contribution. Too high a level might dissuade some employees from participating, while too low a level might result in some motivated pension savers actually saving less than they would otherwise save. I return to this issue below.

Another paper (Choi et al (2001)) comes to the same conclusion as the one discussed above. They, neatly, summarise their conclusions by noting that employees very often take “the path of least resistance”. This suggests that policymakers can strongly influence the pension saving outcomes of individuals by determining the default option, which will be the path of least resistance. At the moment, for employees of firms who do not have a pension scheme (and for many who do), the default is not to save for a pension. By switching this default, the Irish government could potentially significantly increase the proportion of people with some private pension provision, while at the same time leaving the choice set of all individuals largely unchanged.

Preliminary UK evidence

The evidence provided by Madrian & Shea, while certainly striking, is based on behaviour of the employees in a single firm, so care must be taken in using their results to predict what might happen in a national scheme. We simply do not know what factors (informal persuasion, culture of the firm, attitudes of its employees, how precisely the change was introduced) might have contributed to the outcome. The success, or otherwise, of the UK policy will, perhaps, be of more interest to Irish policymakers.

Data on enrolment in the new scheme that is fully representative of employees and firms in the UK is not yet available, not least because only the largest employers are so far obliged to operate the scheme. However, the Department for Work and Pensions (2013) has released a preliminary analysis of some data, which show that an average of only 9% of employees opted out of the scheme in the first month of its operation, with the proportion of those opting out by the third month being approximately 11%.

There are a number of caveats to the interpretation of this number. These include the preliminary nature of the analysis, the fact that these employers, being the largest, are not representative of all employers and the fact that the minimum employee contribution is very low (1%) until 2017 at which point it will start to rise to 4%. However, the very low-opt out rates, combined with evidence provided by Madrian & Shea, do indicate that automatic enrolment can dramatically increase the proportion of individuals saving in a pension.

These numbers refer to proportion participating in the scheme, not the level of their contributions. There is, as yet, no publicly-available data on the level of contributions made by members of the new scheme.

It is tempting to assume that the high rates of participation are due exclusively to auto-enrolment. However, for most of the new pension savers, their employer didn’t previously offer a workplace pension, let alone an employer contribution. The administrative and psychic costs associated with setting up one’s own pension are likely to be substantial for many individuals. Further research is necessary to try to assess whether the small numbers opting out are due to auto-enrolment per se, the provision of the workplace pension or the matched employer contribution. It is likely that each of these factors played some role.

3 Issues to consider

This section discusses a number of design issues that will need to be faced should the Irish government establish a similar scheme.

Default fund

It is likely that many new pension savers under a scheme of auto-enrolment will not be particularly well-versed in financial markets and may feel unprepared to make a decision over which funds their pension savings are invested. There is evidence that when individuals are presented with a large number of choices they can become overwhelmed, and unable to select one of the options facing them, they choose none. This phenomenon has been called, variously, Choice Paralysis, Overchoice and The Paradox of Choice (see Tversky & Shafir 2002, Schwartz 2004).

To balance the objectives of giving pension savers who want to make a choice over investment allocations such a choice and not discouraging those who don’t want to make a choice, a menu of funds will need to be provided, with a default fund for those who choose not to make an active decision.

The approach taken by the National Employment Savings Trust (NEST) in the UK with regard to the default fund combines a standard approach to pension fund management (‘lifestyling’) with an innovative addition (‘foundation stage’). ‘Lifestyling’ involves decreasing the riskiness (and therefore the expected return) of the portfolio held by an individual as they get closer to retirement age. The ‘foundation stage’ has been added due to a concern that, if large nominal losses are realised within the first few years of the introduction of the policy, new pension savers may get discouraged and opt-out. NEST’s foundation stage involves keeping the risk low with a view to ensuring nominal growth in the first number of years of membership4.

Keeping the management fees of the default fund low would be an important part of any auto-enrolment scheme. Passive management of the default fund would be one way to ensure this. A perception that excess returns are being earned by the providers of the pension schemes into which employees are auto-enrolled would be damaging, not only to the pension wealth of scheme members (if the perception is valid), but also to the legitimacy of the scheme and the likely rates of participation. The performance of the (non-profit) NEST in the UK will deserve some study should a similar scheme be introduced in Ireland.

The default level of contributions

Care needs to be taken in setting the default level of contributions. Too high and the proportion staying in might be detrimentally affected; too low and the level of the pension achieved by those choosing the default level will be more modest.

Further, it can’t be assumed that those already doing some pension saving will not be affected by the choice of default contribution rate in a new national scheme. It was noted above that, in the firm studied by Madrian & Shea, there was evidence that some individuals who were previously making pension contributions of greater than the default contribution rate reduced their contributions to that default level – perhaps seeing the default level as a recommended level.

In the UK the total default contribution including both tax relief and employer contributions will be 8% (for basic rate taxpayers)5 when the policy has been completely phased in, although, as noted above, the initial levels are lower. The appropriate rate of pension saving is different for those with different levels of income. The lower are earnings, the greater is the share of pre-retirement income that is replaced by the state pension and therefore the lower will be the rate of pension saving that is needed to obtain a given replacement rate in retirement. So the level of 8% may be more appropriate for lower lifetime earnings individuals than for higher lifetime earnings individuals. Calculations about retirement resources that rely on future state pension income rely, of course, on an assumption that the state pension (generous in Ireland compared to the UK) is not squeezed as demographic pressures mount.

Regular statements with realistic projections about likely levels of pension income may help inform scheme members, as long as they are appropriately and intuitively constructed. However, given that the introduction of auto-enrolment has been introduced in the UK to overcome supposed inertia in individuals’ decisions to start pension saving, one might consider that a similar type of inertia might prevent them from increasing contribution levels beyond the default level. Automatically increasing levels of contribution with tenure in the scheme or at the time of pay increases might prove an effective manner of increasing the level of pension contributions from those who initially joined at a lower level.

A scheme known as ‘Save More Tomorrow’, in which employees are asked to commit to increasing their pension contributions when they receive future pay increases has been shown by Thaler and Benartzi (2004) to drastically increase the level of contributions.This is the case even though the employee retains the right to change their mind – that is the commitment that they give is a ‘soft’ one. In effect they are changing the level of contributions that will be made if they make no active decision at the time of their pay increases. Combining a default rate that is initially low, and subsequently escalating, may be a mechanism of achieving high levels of participation in a scheme at medium to high contribution rates.

Employer contribution

One crucial decision that might affect both the tendency to contribute and the likely pension pot that participants will have is whether there would be a compulsory employer contribution for those employees who participate. An employer contribution of 3% is planned in the UK scheme. An employer contribution would likely increase rate of participation but would act like a tax on employers and should be analysed as such. It should not be assumed that any employer contribution will necessarily account for extra remuneration in the long run. Even if employers are prohibited from reducing pay for those who participate (effectively turning the employer contribution into an employee contribution), there would be nothing to stop the employer taking into account the effect of this new ‘tax’ on their ability and willingness to award future increases in the basic rate of pay.

Dealing with opters-out: should everyone be increasing their pension saving?

It is not necessarily the case that everyone should be increasing their pension saving. There are a number of categories of individuals for whom pension saving should not be a priority. These include those who have adequate (or perhaps more than adequate) resources for retirement6, those who are actively paying off debt that is subject to very high rates of interest and some of those who are trying to save for a property deposit.

This point is made to emphasise that the target for participation should not necessarily be 100% (if it were, then compulsory pension saving might be considered a more attractive proposition). That said, should a scheme be introduced in Ireland, surveys of those who opt-out would be extremely valuable. This could assess whether those opting-out are doing so for sound financial reasons or otherwise. More ambitiously, pilot studies of different approaches to reducing opt-outs might be trialled.

Lloyd (2014) suggests some interesting ideas for encouraging participation among those who opt-out. These include targeted financial management courses, bonuses for those who join and regular statements showing those who have opted out how much they have foregone in employer contributions and tax relief by not participating.

4 Conclusion

‘Auto-enrolment’ involves enrolling all employees into a pension scheme without compelling them to remain in it. It has been suggested that it might be a useful reform in Ireland. This short commentary describes the policy, introduces some evidence on how it has dramatically increased the proportion saving in a pension elsewhere and outlines some issues that would need to be considered if such a policy was to be introduced in Ireland.

Auto-enrolment has many attractive features – especially the likelihood (if the fact that small proportions opting out in the UK could be replicated in Ireland) that many more people will start pension saving while avoiding any compulsion.

In spite of that, this commentary is not unambiguously advocating such a policy. A firm recommendation on policy would require first – a comprehensive analysis (that takes into account likely state pension income) of the extent to which there is an under-saving problem in Ireland and if so among whom and second – an investigation of the alternatives to auto-enrolment – in particular compulsory pension saving.

References

Schwartz, B. (2004). The paradox of choice: Why less is more. New York: Ecco

Choi, J.J, Laibson, D, Madrian, B. & Metrick A. (2001) “Defined Contribution Pensions: Plan

Rules, Participant Decisions, and the Path of Least Resistance,” NBER Working Papers 8655,

National Bureau of Economic Research, Inc.

http://finance.wharton.upenn.edu/~rlwctr/papers/0201.pdf

Crawford, R. & O’Dea, C. (2012), ‘The adequacy of wealth among those approaching retirement’, Institute for Fiscal Studies Report No. 72. IFS: London

http://www.ifs.org.uk/publications/6403

Department for Work and Pensions (2013), ‘Automatic Enrolment evaluation report’ – Research Report No 854, DWP, London.

https://www.gov.uk/government/uploads/system/uploads/attachment_data/file/261672/rrep854.pdf

Lloyd, James (2014), “Beyond Auto-enrolment – Eligible non-savers and the opt-out opportunity”, Strategic Society Centre, London.

http://www.strategicsociety.org.uk/wp-content/uploads/2014/01/Beyond-Auto-enrolment.pdf

Madrian, B.C. & Shea, D.F, (2001) “Inertia in 401(k) Participation and Savings Behavior”. The

Quarterly Journal of Economics, Vol. 116, No. 4 (Nov., 2001), pp. 1149-1187

Pensions Policy Institute (2012) “What are the lessons from KiwiSaver for automatic enrolment in the UK?”. Pensions Policy Institute Briefing Note 62.

http://www.pensionspolicyinstitute.org.uk/briefing-notes/briefing-note-62-what-are-the-lessons-from-kiwisaver-for-automatic-enrolment-in-the-uk

Thaler, Richard H. and Benartzi, Shlomo, (2004), Save More Tomorrow (TM): Using Behavioral Economics to Increase Employee Saving, Journal of Political Economy, 112, issue S1, p. S164-S187,

Tversky, Amos and Eldar Shafir (1992). “Choice Under Conflict: The Dynamics of Deferred

Decision.” Psychological Science, 3: 358-361.

Notes:

1 I am grateful to Donal de Buitleir, Anne Maher, Garry O’Dea and Mary Walsh for useful comments. Any opinions expressed here are those of the author and not those of the Institute for Fiscal Studies or PublicPolicy.ie. Correspondence to cormac.odea@ifs.org.uk

2 In these models individuals may see the virtue of performing some activity that imposes costs today (such as saving). However, they make decisions in a manner that is described as “time-inconsistent”. That is they indulge their current self (by not saving) justifying this decision by deciding (and believing) that their future self will start saving (say next month). This belief is erroneous. Their future self is just as inclined as their current self to defer the decision to save into a pension and they postpone the decision once again.

3 Further information is available from the UK Pension’s regulator.

4 The NEST description of the default funds notes that: “During our research younger savers told us that they may stop saving if they see falls in the value of their retirement pot. This is true even for short-term or one-off losses. For this reason we focus on steady nominal growth rather than the ambitious targets of the growth phase.”

5 This comes from an employer contribution of 3%, an employee contribution of 4% and tax relief on the latter that accounts for an additional 1% of salary.

6 A summary of the scheme and its implications can be found here.

Tagged with:

Pensions

About author

Related Articles

-

-

Ireland’s Pension System Assessed

6 Nov 2017 -

Social Protection – Expenditure Trends

28 Aug 2017 -

79 Merrion Square, Dublin 2, Ireland

tel: 353 (1) 676 0414 | email: info@publicpolicy.ie

Company registration number: 504956

Privacy Policy | Chairman's Blog | Events | Video | Public Policy Documents | News Property Tax Ireland | Pension Reform Ireland | Water Charges Ireland