{kind=link}

Work Incentives

23 Jan 2014Introduction

A key aim of public policy is to ensure that work pays while achieving adequate income protection for the unemployed. This is particularly important in the case of young people in order to avoid locking them into long-term unemployment which has very negative economic and social consequences in the longer-term.

What does the data tell us about how we reconcile the need to provide adequate social protection with that of ensuring that disincentives to enter or rejoin the labour market are minimised? The EU has published very useful data on this question in a recent publication1 .

Labour Market Performance

The employment rate of low-skilled workers2 in 2012 was as follows

Ireland 47.1%

EU 27 62.1 %

Ireland ranking 24

We are one of the worst performing EU Members states on this measure. Only Slovakia, Bulgaria and Lithuania are worse. So we have a problem in that about half of our low-skilled workers are unemployed.

Definitions

Economically inactive people are those who are not in work, but who do not satisfy all the criteria for unemployment under the International Labour Organisation (ILO) convention (wanting a job, seeking a job in the last four weeks and available to start work in the next two), such as those in retirement and those who are not actively seeking work. Unemployed people are those who meet the ILO criteria.

Work Incentives

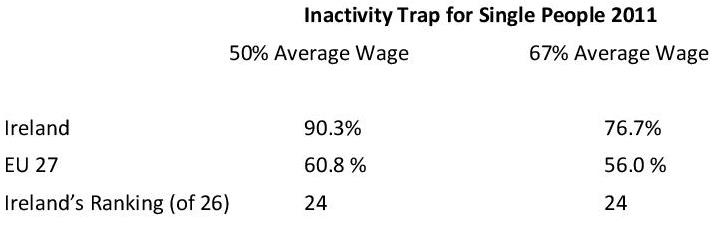

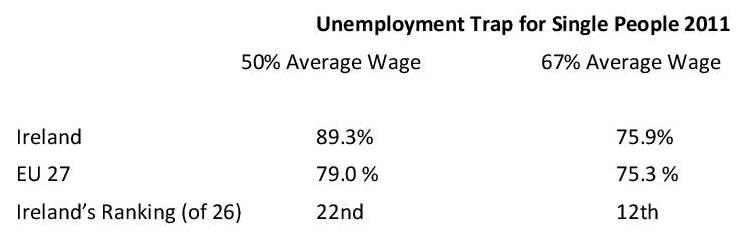

The EU report uses two measures to assess work incentives. These are the inactivity trap3 and the unemployment trap4 . The data is as follows

Only Denmark and Netherlands are worse

At the 50 % level only Luxembourg, Netherlands , Denmark and Poland are worse.

The contribution of the tax system to these implicit marginal tax rates is very low by European standards (less than 3% in the case of the inactivity trap and about 10 % for the unemployment trap); the problem seems to be arising from the loss of benefits.

Such high effective marginal tax rates are at levels that would be unconscionable if applied to those at the top of the income distribution; why is this not the case at the other end of the income distribution ?

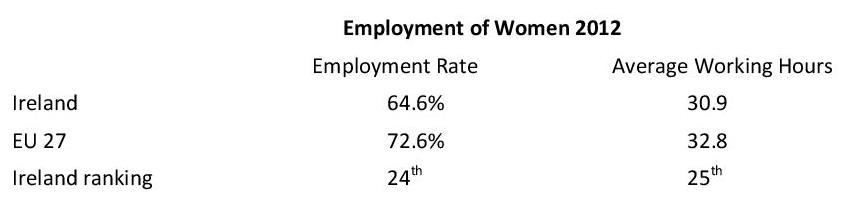

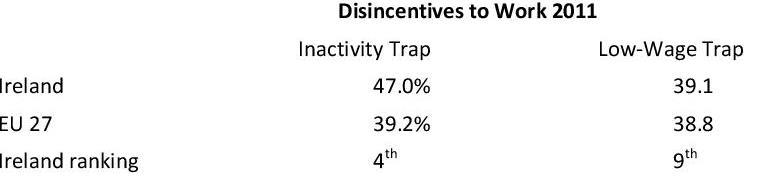

Second Earners

Second earners sometimes face specific disincentives to returning to work from inactivity or to increasing the number of hours worked. Such disincentives usually arise from the tax system but loss of benefits can also play a role.

The employment rate and average hours worked for women (used as a proxy for second earners) is as follows

Note: Employment rate is for age group 25-54. Female working hours refers to average number of usual weekly hours of employed persons in main job.

Note : The inactivity trap is for second earner in a two earner couple with two children; principal earner with 67 % of average wage , second earner with 67 % of average wage.

The low-wage trap is for second earner in a two earner couple with two children; principal earner with 67 % of average wage, second earner moving from 33% to 67 % of average wage.

In Ireland about a quarter of the disincentive is due to the tax system compared with an average of about 40% in EU countries.

Conclusion

Based on this data the disincentives to work for young people with low skills are high and need to be reduced. While the issue is clear, it is less obvious what to do about it. One route, not likely to be acceptable is to reduce benefits. Another is to extend the earnings taper. This looks more attractive but it pushes the traps further up the earnings distribution and is more costly. Another option is to make an in-work benefit like Family Income Supplement more generous and increase the take-up rate. These issues are being considered by the Advisory Group on Tax and Social Welfare which is due to report on the question of in-work support by end June, 2014.

Notes:

1 Tax Reforms in EU Member States 2013, European Economy 5/2013

2 Low-Skilled workers are those aged 25-54, with only pre-primary, primary or lower secondary education

3 Inactivity trap refers to the disincentive to return to employment after inactivity. The inactivity trap is also often referred to as the participation tax rate and refers to the part of the additional gross wage that is taxed away in the form of increased taxes (personal income tax, employee social insurance contributions) and withdrawn benefits such as unemployment benefits, social assistance and housing benefits in the event of an inactive person taking up a job.

4 Unemployment trap refers to the disincentive to return to employment from unemployment. It measures the part of the additional gross wage that is taxed away when a person returns to work from unemployment. It takes into account the reduction in benefit payments following the return to the labour market, as well as higher taxes and social insurance contributions.

Image: William Murphy.

Tagged with:

Employment

About author

Related Articles

-

-

Involuntary Part-time Work

28 Jun 2017 -

Where Do The Jobs Come From?

9 Feb 2017 -

79 Merrion Square, Dublin 2, Ireland

tel: 353 (1) 676 0414 | email: info@publicpolicy.ie

Company registration number: 504956

Privacy Policy | Chairman's Blog | Events | Video | Public Policy Documents | News Property Tax Ireland | Pension Reform Ireland | Water Charges Ireland