{kind=link}

Environmental And Income Taxes

24 Aug 2016Key Point

Environmental taxes are seen as one of the least distortionary taxes. Ireland’s taxes on pollution and resources are one third of the EU average. There may be scope to address this issue by decreasing direct taxes on labour and increasing taxes on pollution.

Introduction

An environmental tax is a tax whose base is a physical unit (or a proxy of a physical unit) of something that has a proven, specific negative impact on the environment. Environmental taxes are more labour friendly than direct taxes on income.

Environmental Tax Revenues

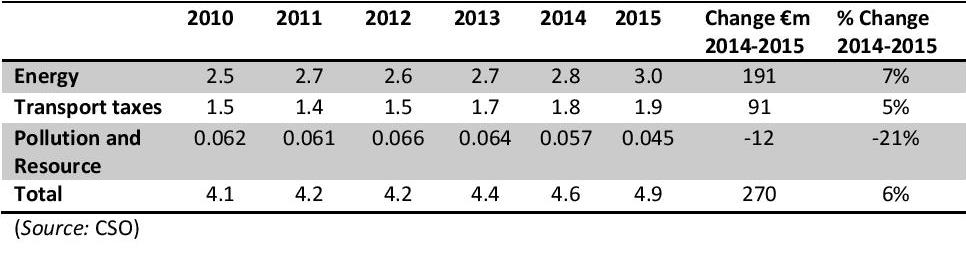

In the ten years from 2006 to 2015, environmental taxes in Ireland have increased by 10% from €4.5bn to €4.9bn, with aggregate revenue of €44bn over the period. As a share of total taxes collected, environmental taxes average 8.2%.

Energy taxes include taxes on transport fuels, such as the carbon tax. Transport taxes relate mostly to motor vehicles, such as VRT and motor tax. In 2015, the majority of revenue from environmental taxes (61%) was attributed to energy taxes, followed by transport taxes (38%), and taxes on pollution and resources (1%). Table 1 shows the data from 2010 to 2015.

Table 1 – Environmental Taxes 2010 – 2015, €billion

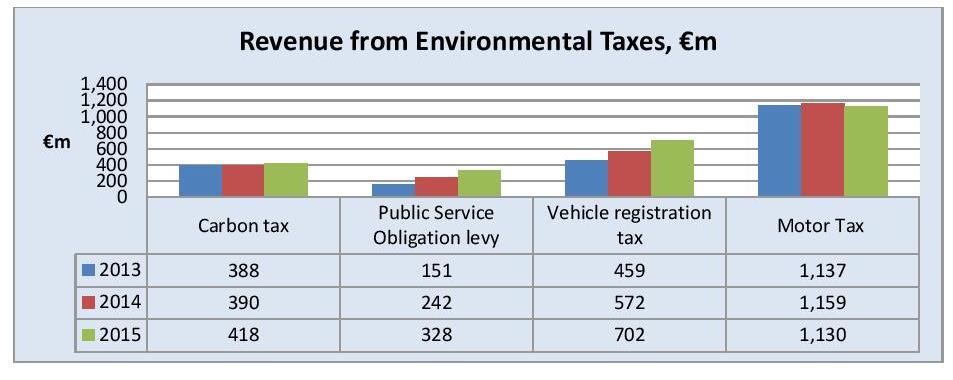

Revenue from energy taxes reached €3bn in 2015; an increase of 19% over 2010. Transport taxes were €1.9bn; an increase of 23% over 2010, while pollution and resource taxes were €45m; a decrease of 28% over 2010. Figure 1 illustrates four environmental taxes and revenue raised between 2013 and 2015.

Figure 1

(Source: CSO)

Over the period 2013 to 2015, carbon tax revenue has increased by 8%, Public Service Obligation (PSO) levy by 117%, VRT by 53%, and motor tax fell by 1%. The energy tax which increased revenue the most in 2015 over the previous year was the PSO levy; increasing 35% (€86m). In terms of transport taxes, VRT revenue increased by 23% (€130m) over the same period reflecting a 30% increase in car sales. Pollution and resources revenue has declined by 21% in 2015 over 2014 (see table 1) as consumers change their behaviour to avoid the plastic bag levy and the landfill levy. The third tax under pollution relates to fisheries protection which accounts for 2.5% of the total tax yield.

Revenue from the plastic bag levy increased marginally in 2015 over the previous year by 6% to €16m, while revenue from the landfill levy reduced by 32% to €28m. The landfill levy is currently set at €75 per tonne of waste (last increased in 2013 by €10 per tonne). The levy has contributed to a reduction in municipal waste per capita of 24% between 2007 and 2013.

Irish and EU Context

Total environmental tax revenues have increased by 15% (€46bn) between 2008 and 2014 in the EU 28. Revenue from taxes on energy have increased the most in percentage terms (19%), followed by taxes on pollution and resources (11%), and taxes on transport (3%). Revenue by category of environmental tax in the EU 28 in 2014 was dominated by energy taxes (76%), followed by transport (20%), and taxes on pollution and resources (4%).

Energy taxes in Ireland made up 61% of total environmental taxes in 2014. This is the sixth lowest share in the EU28 and 20% below the EU 28 average. Ireland had the second highest share of transport taxes at 38% of total environmental taxes. Only Malta had a higher share of transport taxes at 41%. Ireland’s transport tax revenues were 91% above the EU 28 average.

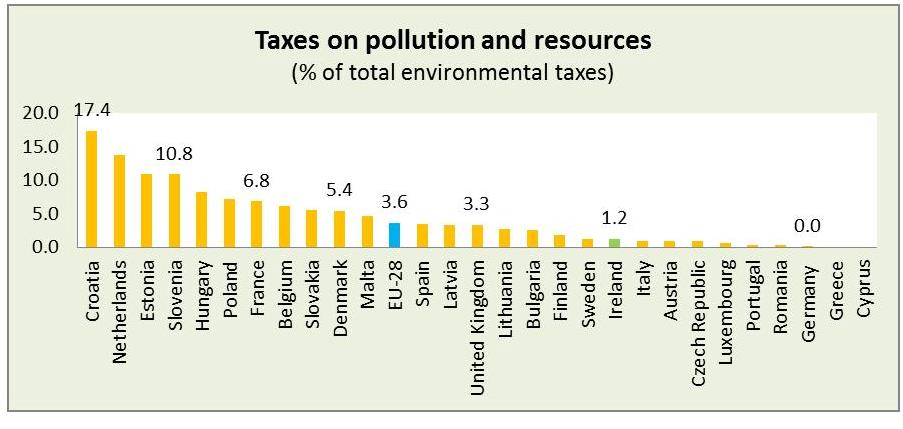

Ireland’s taxes on pollution and resources made up 1.2% of total environmental taxation. This is the seventh lowest in the EU 28 and one third of the EU 28 average of 3.6%. Taxes on pollution include taxes on greenhouse gas emissions, effluents to water, and waste management. Taxes on resources include water abstraction and extraction of raw materials. Figure 2 illustrates the wide range in the share of pollution and resource taxes across the EU.

Figure 2

(Source: Eurostat)

Ireland’s non-emission trading scheme (non-ETS) greenhouse gas (GHG) emissions are projected to exceed annual EU binding limits every year up to 2020. Agriculture and transport are expected to account for 47% and 29% of non-ETS GHG emissions by 2020 respectively. Addressing this challenge may require further environmental taxation to discourage GHG emission production.

Income and Environmental Taxes

Pollution taxes in the EU cover emissions to air and water, and waste management. Resource taxes relate to the extraction or use of natural resources. It appears that pollution and resource taxes in Ireland are relatively narrow. However, the Carbon Tax (introduced in 2010) does capture environmental damage caused by the production of energy and use of transport. Increasing pollution and resource taxes could provide scope to reduce income tax or USC.

About author

Related Articles

-

-

Low Tax Burden On Labour In Ireland

29 Nov 2017 -

-

Reforms to Boost Growth

12 Apr 2017

79 Merrion Square, Dublin 2, Ireland

tel: 353 (1) 676 0414 | email: info@publicpolicy.ie

Company registration number: 504956

Privacy Policy | Chairman's Blog | Events | Video | Public Policy Documents | News Property Tax Ireland | Pension Reform Ireland | Water Charges Ireland