{kind=link}

Should First-Time Buyers Get Help To Save For House Deposits?

24 Mar 2015Key Point

Consideration should be given to introducing a scheme which would help first-time buyers save the funds for a house deposit out of taxed income.

The New Rules

In February, 2015 the Central Bank introduced new regulations which apply limits on the proportion of mortgage lending at high loan-to-value (LTV) and high loan to-income (LTI) ratios by regulated financial services providers in the Irish market. The purpose of the regulations is to increase the resilience of the banking and household sectors to the property market and to reduce the risk of bank credit and housing price spirals from developing in the future.

Principal Dwelling Homes For non-first time buyers of primary dwelling homes (PDH),: a limit of 80 per cent LTV applies on new mortgage lending. For first time buyers (FTBs) of PDHs: a limit of 90 per cent LTV applies on the first €220,000 of the value of a residential property and a limit of 80 per cent LTV applies on any value of the property over €220,000. In this way, FTBs purchasing more expensive properties will be subject to a lower maximum LTV ratio than those purchasing cheaper properties. Housing loans for borrowers in negative equity who wish to obtain a mortgage for a new property are not in scope of the LTV limits.

The LTI limit of 3.5 times gross annual income applies to all new lending for PDH purposes. The LTI limits do apply to borrowers in negative equity who wish to obtain a mortgage for a new property.

Financial institutions will be allowed to make a limited number of loans which exceed these limits.

The new rules are important in preventing the emergence of another housing bubble and are welcome. However, consideration should be given to introducing a scheme which would help first-time buyers accumulate the necessary funds out of taxed income.

First-Time Buyers

Concerns have been expressed that the need to have deposits saved may make it difficult for some first-time buyers to acquire a home. For example, the Department of Finance in its submission on the original proposals noted

“For those households who have to save an increased deposit while also paying market rents, the proposed LTV rules could make it much more difficult (or even impossible) to secure a mortgage even in circumstances where there is a clear capacity to repay a mortgage based on a more normal deposit or other reasonable mortgage requirements and which the household can demonstrate a track record by meeting comparable, or possibly in some cases, higher rental payments.”

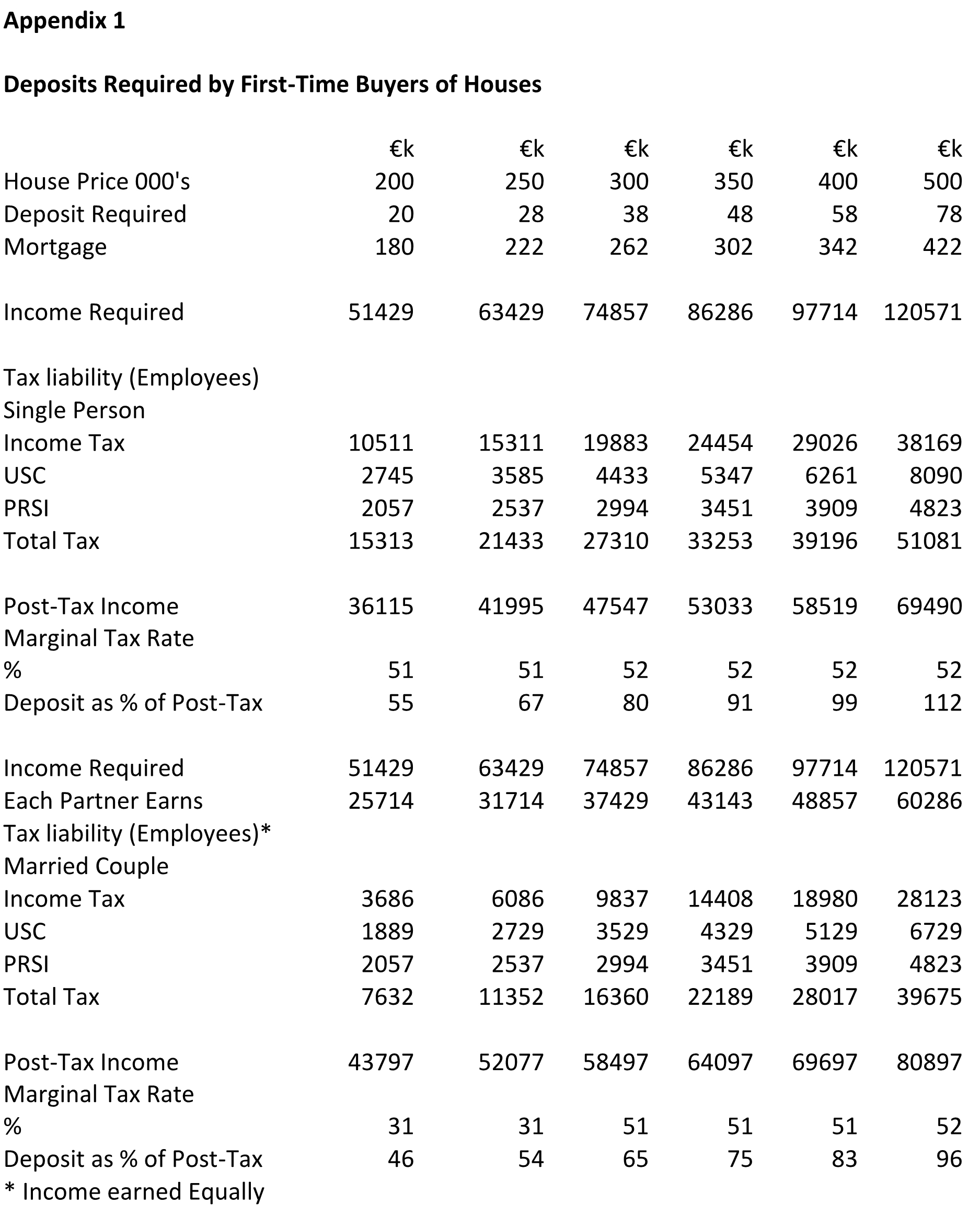

Under the new regime the deposits required range upwards from about half of annual income. See examples in Appendix 1.

The existence of high marginal tax rates at relatively low levels of income makes it difficult to accumulate savings of this magnitude out of taxed income. For example, a single person earning €40,000 pays a marginal tax rate of 51 per cent. To buy a house costing €250,000 will require a young couple to have savings of €28,000. Given high tax rates and rental costs unless a couple have access to other resources such as gifts from parents, it could take them some time to save this amount of money. For example, when half of marginal income has to be paid in taxes, the amount of pre-tax earnings necessary to save €28,000 is €56,000.

One possible means to assist those aspiring to buy their first home would be to provide a tax credit for savings in designated accounts to be used for house purchase by first-time buyers on the lines of the SSIA scheme introduced in 2001. A limit on the amount allowed in the account and the associated tax credit could be prescribed. The amount of the tax credit could be set between 25 and 50 per cent. This would be akin to the tax relief accorded to people to acquire another long-term asset i.e. a pension.

A better alternative, particularly if a mandatory or auto enrolment system is introduced for pensions, would be to allow first–time buyers to access some of their accumulated pension savings. The Singapore Central Provident Fund allows this and provides an example of what can be done in this area. This would also encourage greater participation by young people in pension schemes.

About author

Related Articles

-

-

Rental Costs Return to Peak Levels in Dublin *

16 Mar 2016 -

Property Tax – Why Dubliners Should Pay More

19 Jan 2013

79 Merrion Square, Dublin 2, Ireland

tel: 353 (1) 676 0414 | email: info@publicpolicy.ie

Company registration number: 504956

Privacy Policy | Chairman's Blog | Events | Video | Public Policy Documents | News Property Tax Ireland | Pension Reform Ireland | Water Charges Ireland