{kind=link}

Reducing The Number Of Taxpayers Increases Risks

8 Mar 2017Key Point

Approximately one-in-three individuals (748,300) are exempt from both income tax and universal social charge (USC) in 2017. Further narrowing of the tax base will increase risks.

Introduction

The European Commission has highlighted the risks of eroding the tax base.

“Relying on a broader tax base would support revenue stability in the face of economic volatility. Ireland has done very little to broaden the bases of its tax heads. Budget 2017 has introduced a range of tax expenditure measures which are likely to narrow the income tax base thereby increasing public finances’ exposure to shocks”.

The Commission goes on to state that Ireland has done very little to broaden the bases of its tax heads and that, “the phasing out of the Universal Social Charge will undermine the commitment to maintain a broad tax base”.

What is the Position ?

Income tax (including USC) accounts for 40 per cent of Exchequer tax revenue, slightly more than that obtained from VAT and excises combined (38.2%)

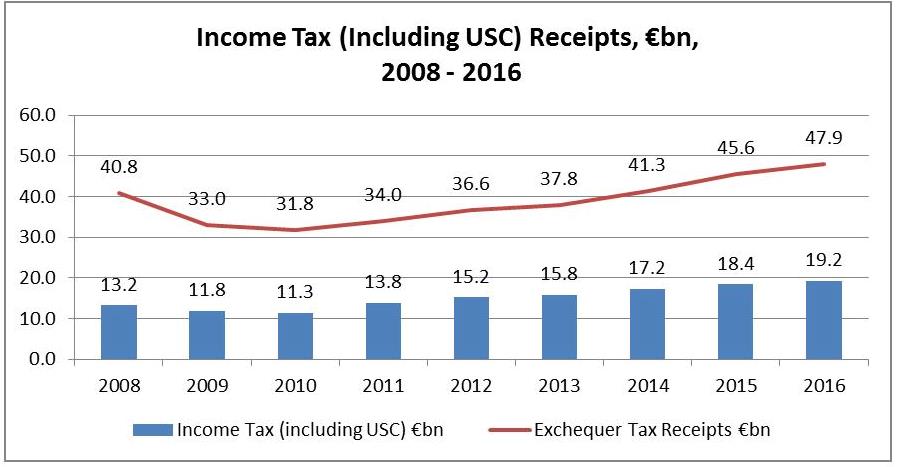

Figure 1 shows exchequer and income tax (including USC) receipts from 2008 to 2016.

Figure 1

(Source: Department of Finance)

Since the low point in 2010, income tax receipts (including USC) have increased by almost 70 per cent through a combination of higher tax rates and increased employment.

Who Pays ?

Of the 2.5 million taxpayer units1 in Ireland in 2017, 43% will pay the standard rate of income tax of 20%. A further 21% will pay the higher rate (40%) of income tax, while over a third (37%) will be exempt from income tax.

In relation to USC, 1.1m (42%) will pay USC at a rate of 5%. A further 484,700 (19%) will pay 2.5%, and 226,900 (9%) will pay 8%. 748,300 (30%) will be exempt from USC.

As a result, 30 percent of income earners are exempt from both income tax and USC.

How Is Income Distributed ?

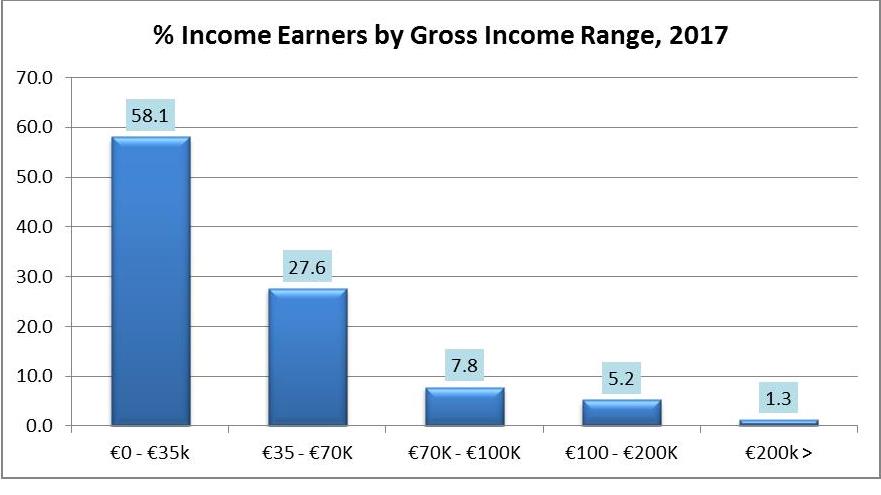

Figure 2 shows the share of income earners grouped under five gross income ranges.

Figure 2

(Source: Revenue Commissioners)

(Source: Revenue Commissioners)

The majority of taxpayer units (58.1% or 1.5m) have a gross income of less than €35,000 in 2017. Those earning €35,000 to €70,000 account for 695,864 (27.6%) of taxpayer units, while 196,041 (7.8%) earn between €70,000 and €100,000. Those earning €100,000 or more account for 163,713 (6.5%) of all taxpayer units.

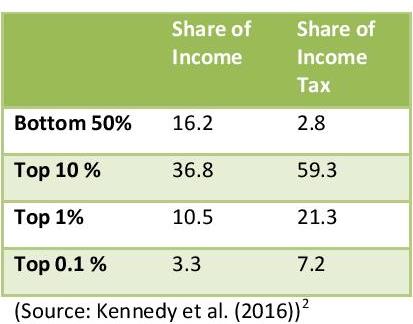

Table 1 shows the dependence on a minority of individuals for the vast bulk of income tax receipts.

Table 1

While choices regarding the distribution of taxes are matters for political decision, further erosion of the tax base such as through abolition of the Universal Social Charge will further increase the concentration of tax revenue and our vulnerability to economic shocks.

________________________________

Notes:

1 Married persons or civil partners who have elected/ determined for joint assessments are counted as one tax unit.

2‘Taxes, Income and Economic Mobility in Ireland’, Kennedy et al. Economic and Social Review, Vol 47.1 Spring 2016

About author

Related Articles

-

-

Low Tax Burden On Labour In Ireland

29 Nov 2017 -

Integration Of PRSI And USC

11 Oct 2017 -

79 Merrion Square, Dublin 2, Ireland

tel: 353 (1) 676 0414 | email: info@publicpolicy.ie

Company registration number: 504956

Privacy Policy | Chairman's Blog | Events | Video | Public Policy Documents | News Property Tax Ireland | Pension Reform Ireland | Water Charges Ireland