{kind=link}

Ireland’s Path towards Fiscal Sustainability

10 Apr 2014Irish fiscal policy is to a large extent shaped by EU legislation, and particularly by the Stability and Growth Pact. The following article compares improvements in the fiscal stance to the requirements of the Pact, and examines potential threats, which could derail Ireland from a path towards fiscal sustainability.

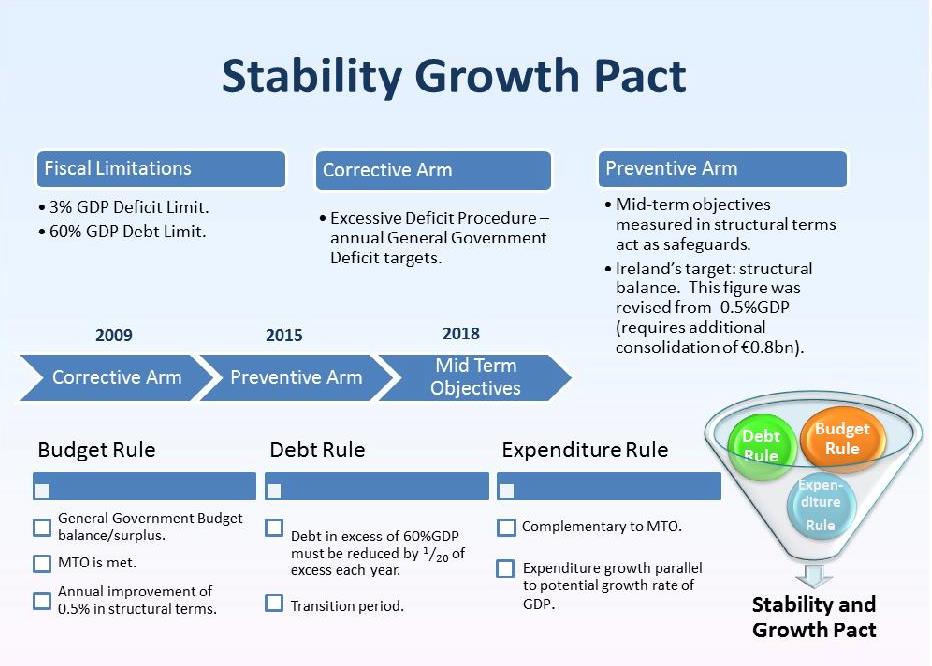

Two conditions form the foundation of the Stability and Growth Pact (SGP):

- Deficit limit of 3% GDP

- Debt limit of 60% GDP.

SGP contains two arms – the corrective arm and the preventive arm.

If a country is in breach of either the debt or deficit limits, it is subject to the corrective arm. The European Council will issue an Excessive Deficit Procedure (EDP), representing annual deficit or debt targets. Failure to comply with these targets could result in sanctions of 0.2% GDP. Alternatively, if a country is not under EDP, it is subject to the preventive arm, a cornerstone of which is the mid-term objective (MTO). The MTO is a country-specific benchmark measured in structural (i.e cyclically adjusted) terms, which every country should aim to achieve. Its purpose is to allow for a safety margin and budgetary manoeuvre in case of adverse unexpected events. In 2013 Ireland’s MTO was revised from a structural deficit of 0.5%GDP to a structural balance. The cause for this revision is Ireland’s exceptionally high debt levels. This tightening in the required structural balance – other things being equal- will require additional consolidation measures of €0.8bn.

Ireland has been subject to the Corrective Arm since 2009, and is scheduled to transition into the preventative arm in 2015, as the deficit is reduced to below 3%. Official estimates show the MTO of structural balance will be met in 2018.

As a result of the Fiscal Treaty, Ireland is required to comply with the three rules.

- The Budget Rule requires that one of 3 conditions is met: the General Government Budget is in balance or surplus; the MTO is met; there is an annual improvement of 0.5% GDP in structural terms.

- The Debt Rule requires that debt levels above 60%GDP decline by 1/20th of the excess annually. However, a transition period allows for a three year break after excessive deficits are corrected, implying that Ireland will be subject to the debt rule from 2019.

- The Expenditure Rule requires that expenditure growth does not exceed potential GDP growth, unless accompanied by tax increases.

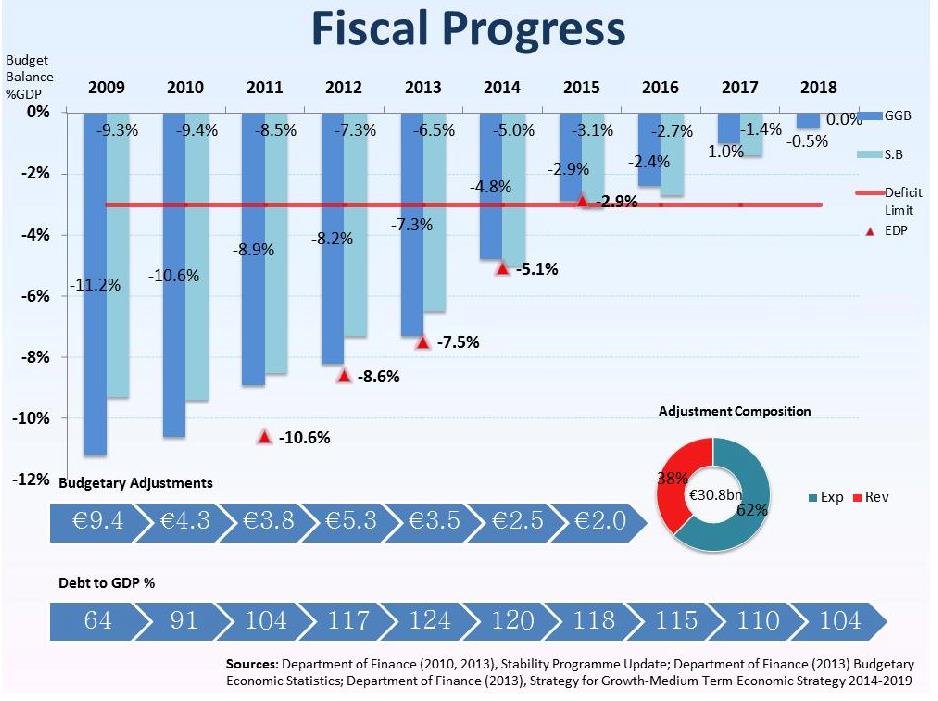

The attached charts illustrate Ireland’s fiscal progress. Three key points require emphasis:

- The General and Structural deficits have been steadily falling. The adjustments required for this are shown below for their respective years. They have a total value of €30.8bn and are composed of 62% expenditure cuts and 38% revenue raising measures

- Ireland has met and over achieved its EDP targets to date.

- Debt-to-GDP ratio is expected to have peaked in 2013 at 124% and then will begin to fall. Debt targets will apply from 2019 as required by the Debt Rule.

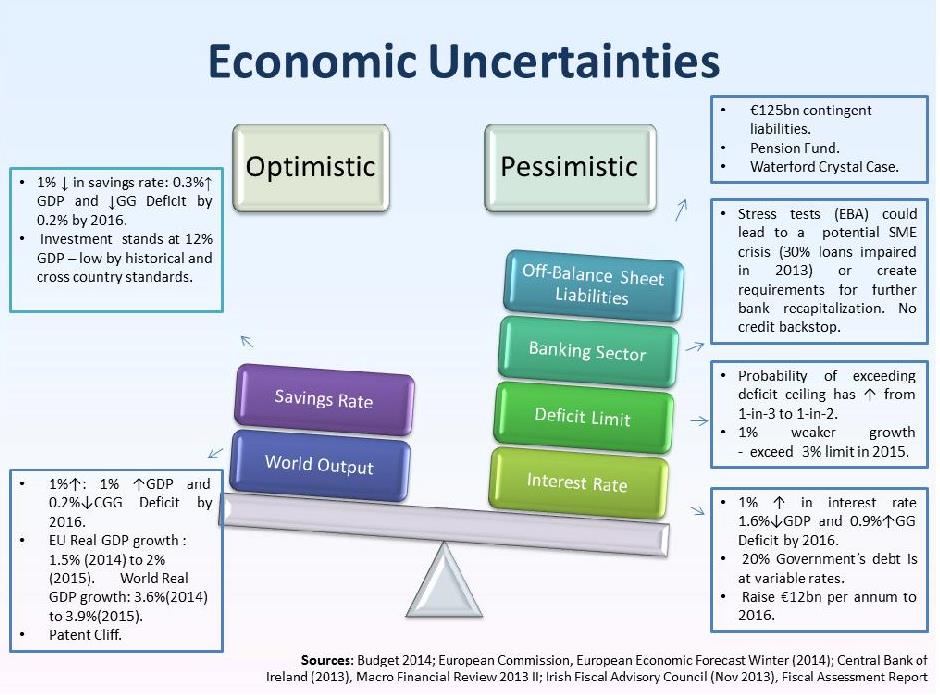

Ireland remains on track to meeting the targets as set out by the Stability and Growth Pact, even if marginally so as is the case in 2015. However, uncertainties include.

- Growth prospects in our trading partners are uncertain.

- A reduction in the savings rate, which in 2013 Q3 stood at 8.4%GDP (CSO, 2014) could boost economic activity. Investment stands at 12%GDP (Dep. Finance, 2013 a), which is low by historical and cross-country standards. A return to investment to normal levels could improve the fiscal position.

- The economy remains vulnerable to increases in interest rates. The state is required to borrow €12bn (IFAC, 2013) per annum to 2016. Household debt is also high. Given the zero lower bound, interest rates present an asymmetric risk.

- The probability of breaching the deficit limit has increased from 1-in-3 to 1-in-2 as a result of the reduction in budgetary adjustments in 2014 (IFAC, 2013).

- Bank stress tests are scheduled to take place this year, carried out by the European Banking Authority. Further bank recapitalization may be required. In the third quarter of 2013, 27% of SME were impaired (Central Bank, 2013

- The Government off-balance sheet liabilities were estimated at €125bn in 2013 (IFAC, 2013).

References:

Central Bank of Ireland (2013), ‘Macro Financial Review 2013 II’.

CSO (2014), ‘Institutional Sector Accounts Non Financial Quarter 3 2013’.

CSO(Dec 2013), ‘Goods Exports and Imports – Dec 2013’.

Irish Department of Finance (2013 a), ‘Budget 2014 Economic and Fiscal Outlook’.

Irish Department of Finance (2013 b), “A Strategy for Growth – Medium Term Economic Strategy 2014-2019”

Irish Fiscal Advisory Council (2013), ‘Fiscal Assessment Report Nov 2013’

About author

Related Articles

79 Merrion Square, Dublin 2, Ireland

tel: 353 (1) 676 0414 | email: info@publicpolicy.ie

Company registration number: 504956

Privacy Policy | Chairman's Blog | Events | Video | Public Policy Documents | News Property Tax Ireland | Pension Reform Ireland | Water Charges Ireland