Budget 2014: The 9% Rate of VAT

11 Nov 2013Introduction

As part of the government’s Jobs Initiative of June 2011, the rate of VAT was reduced from 13.5% to 9% on a range of goods and services, including accommodation, restaurants, and certain cultural activities. The cost of this initiative was estimated to be €350m a year. The policy was initially designed as a temporary measure, and was due to expire at the end of 2013. However, the government decided to extend the lifetime of the 9% rate as part of Budget 2014. This note examines the evidence regarding the effectiveness of the rate cut as a job-creation tool.

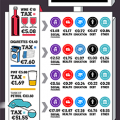

The following is a list of goods and services selected for the rate reduction:

Effectiveness

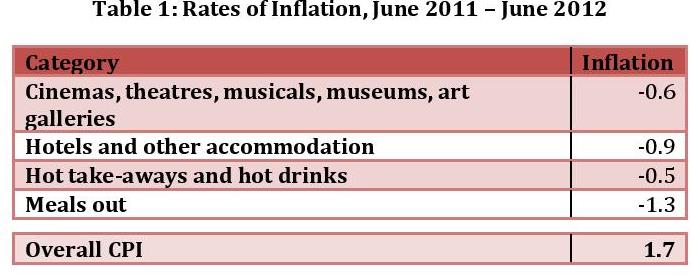

The evidence is considered in greater detail below, but I will draw out some of the main conclusions here. There is evidence that the lower rate of VAT was passed on in part to consumers via lower prices, but this does not appear to have had a significantly positive impact on tourism revenues. The small recovery in the tourism market observed over the second half of 2011 and in to 2012 is more likely to have been influenced by the weakening of the euro than by the relatively minor price changes brought about by the reduced rate of VAT.

Estimates of job creation vary greatly – from 5,600 to 35,000 jobs retained or created – depending on what assumptions are made to fill the void left by the lack of hard data. In his Budget Speech, the Minister for Finance claimed the policy had created 15,000 jobs. However, there are good reasons to believe that these estimates exaggerate job creation attributable to the lowering of the rate of VAT. First, given the relatively weak increase in tourism revenues between 2011 and 2012, this job creation was funded more by changes in the pattern of domestic expenditure rather than by foreign visitors. Domestic consumers can only spend their money once, so that increased spending on goods and services affected by the VAT cut must come at the expense of reduced spending elsewhere in the economy. Estimates of the impact of the reduced rate of VAT fail to consider the possibility of a displacement effect that could damage job creation and retention in other sectors. Because the VAT cut was aimed at sectors that are labour-intensive, the net gain is still likely to have been positive, but the gross gain may exaggerate the effectiveness of the policy.

Second, to the extent that employment benefited from increased tourism numbers, the reduction in the rate of VAT coincided with a weakening of the euro that made holidaying in Ireland relatively more attractive. Because of the timing of these events, their relative influence on tourism and employment creation is difficult to disentangle. However, this exchange rate effect was more significant from a price competitiveness perspective than the pass-through from the VAT cut, and yet is not accounted for in the studies on the impact of the 9% rate.

Opportunity Cost

Determining whether or not the policy was effective is simply the first part of policy analysis; the second part is to determine whether or not it is the best policy for achieving the objective of greater job creation. This is especially important given the scarce resources available to government, and a price tag of €350 million represents a significant investment by government that otherwise could be used to avoid an increase in other taxes, to reduce the deficit or spent on other items.

An obvious alternative policy choice would be to reduce the cost of creating and retaining jobs by lowering taxes on labour directly, rather than the indirect route of encouraging consumption of goods and services that have a high labour content. Economic theory, for what it’s worth, suggests the direct approach would be more effective and less distortionary. It is unfortunate then that another Jobs Initiative policy which made it cheaper for firms to employ people by reducing the lower rate of employers’ PRSI from 8.5% to 4.25% was not retained in Budget 2014

Annex: Reviewing the Evidence

The goal of the 9% rate of VAT is two-fold:

- To encourage more tourists to come to Ireland by lowering the cost of key tourism services,

- To create employment by reducing the tax burden on labour-intensive industries.

When inquiring as to whether or not the policy was effective, we must ask the following questions:

- Was the rate cut passed on to consumers in terms of lower prices?

- Did the lower rate of VAT help attract more holiday-makers?

- Did the revenue of the Irish tourism sector improve?

- Were jobs retained or created as a result?

1. Promoting Tourism

The Theory

The idea behind the policy of reducing VAT on tourism-related products is that it would allow businesses in the tourism sector to increase revenue by passing on the reduction in terms of lower prices and thus attracting more tourists to Ireland. Because of the supposed high elasticity of demand for tourism services – meaning for a given reduction in price, the demand response will be proportionately greater – the increased revenue for businesses should be larger than the cost to the government in terms of lost VAT revenue, so that society as a whole would be better off.

This theory is not without its critics. In their ESRI Working Paper “UK Tourists, The Great Recession and Irish Tourism Policy” Richard Tol and Niamh Callaghan cast doubt on whether or not the response of tourists to lower prices would be greater than the cost to the exchequer. They estimate the demand for Irish tourism from the UK (our single largest market) and find that reducing the rate of VAT (and assuming full pass-through) for accommodation, restaurants and recreational services would increase spending by UK tourists by €20-34 million, compared to forgone VAT revenue of €43 million.

Price pass-through

The first step in determining whether or not the policy had any effect on tourism revenues is to ascertain if prices fell in the tourism sector following the rate cut. In “Measuring the impact of the Jobs Initiative: Was the VAT reduction passed on and were jobs created?” Brendan O’Connor of the Economics Division in the Department of Finance finds some evidence of price reductions in the year following the introduction of the 9% rate, despite rising prices elsewhere in the economy. This implies that the VAT reduction was to some extent passed on to consumers.

Exchange Rate Movements

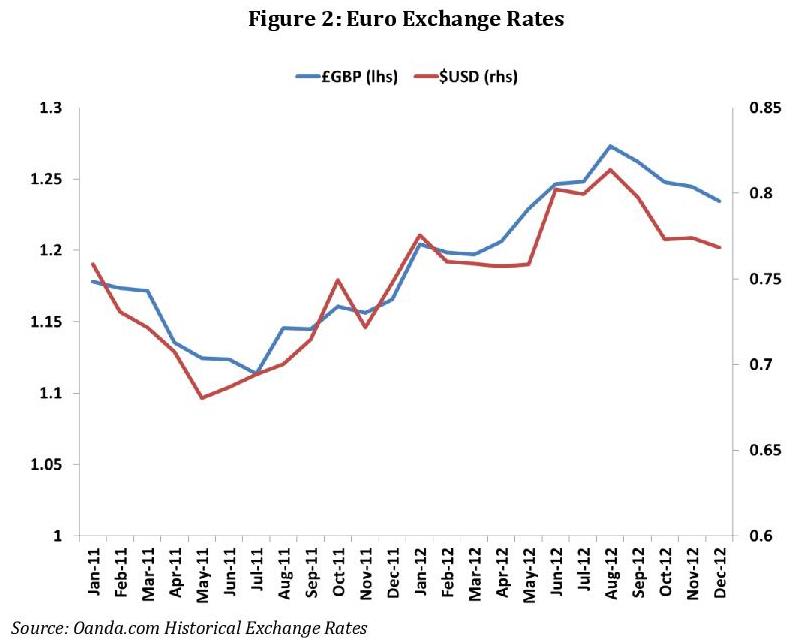

It is unfortunate – from the point of view of isolating the causal effect of lower prices due to the rate cut on tourism – that the Jobs Initiative coincided with a significant weakening of the euro versus both the dollar and the pound. As can be seen in Figure 2, the exchange rate started weakening against both currencies in the summer of 2011 and continued to do so until August 2012. This had a large impact on the purchasing power of foreign visitors – for example, someone who visited Ireland in both July 2011 and July 2012 would find that prices had dropped 13% in dollar terms, or 11% in terms of pound sterling. Compared to the improvement in purchasing power, the reductions in price from Table 1 appear quite small, and are likely to have had less of an effect on tourism numbers.

Tourism Numbers

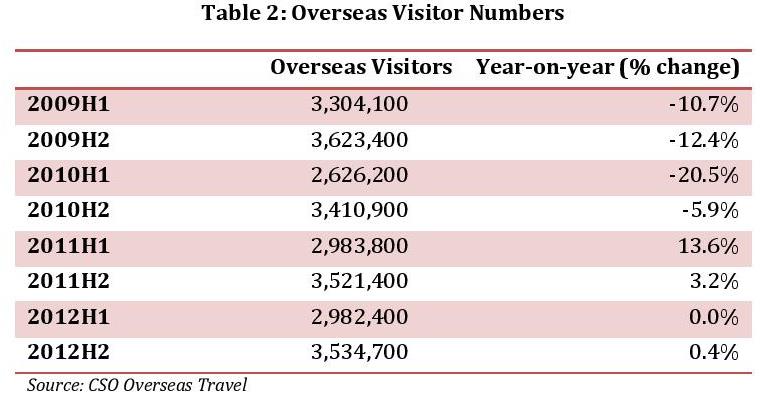

When looking at the data on the number of tourists coming to Ireland, it is important to note that the counterfactual – that is, what would have happened if the policy had not been introduced – is never observed. The data do not show a substantial increase following the introduction of the 9% rate of VAT in June 2011, but it may be argued that policy action prevented the decline that had been occurring since 2008 from continuing.

Tourism numbers in 2011 were up by 7.8% on 2010, but much of this increase occurred before the Jobs Initiative was introduced in June. Comparing the second half of 2011 with the second half of 2010, tourism numbers grew by 3.2%. In 2012, tourism numbers grew by only 0.2% compared to 2011.

Tourism numbers have grown strongly so far in 2013, up 6% on last year. But, while the impact on these numbers of the measures introduced in the Jobs Initiative may be positive, it is difficult to disentangle from the effects of The Gathering (a large-scale marketing campaign aimed at attracting those with roots in Ireland), and so I restrict the analysis to the 18 month period immediately following the VAT cut.

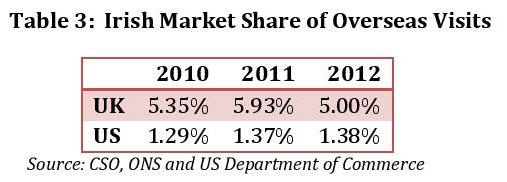

Market Share

Overseas visitor numbers do not by themselves tell the full story. Ireland competes with other countries for market share of international travellers, but the supply of international travellers is not fixed. Economic conditions in their home country can dissuade or encourage individuals to travel. It is therefore instructive to look at the Irish market shares from a couple of our key markets.

UK: Around four in ten visitors to Ireland come from the United Kingdom, making it by far the largest single market for Irish tourism. In 2011, the Irish market share of overseas trips by UK residents rose from 5.35% to 5.93%. But all of the gains were made in the first half of the year, before the reduced rate of VAT was introduced. The improvement in market share coincides with the visit of the British queen, which may be an explanatory factor. The improvement was undone in 2012 as market share fell to 5%.

US: Another important market for Irish tourism is the US, which makes up around 15% of total trips to Ireland. Irish market share for US visitors also rose in 2011 – from 1.29% to 1.37% – but as with UK market share, the increase was mostly seen in the first half of the year, coinciding with the visit of the American president. In 2012, market share improved slightly, rising to 1.38%.

Tourist Expenditure

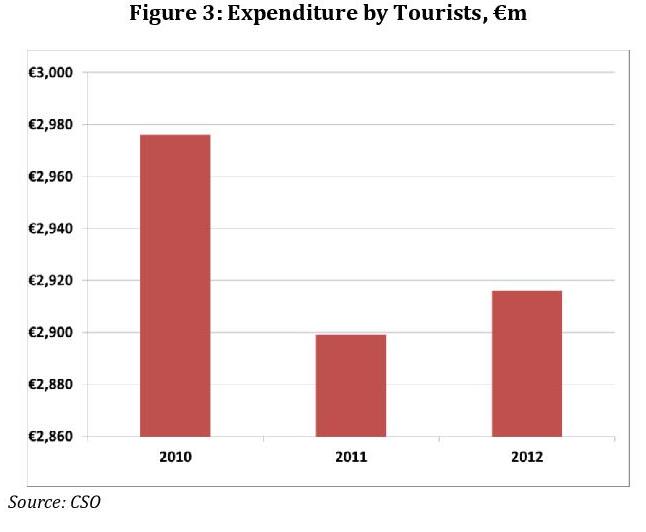

The third question raised above was whether or not the rate reduction led to improved tourism revenues. Figure 3 below shows how expenditure by tourists in Ireland is estimated to have fallen since 2010. This is perhaps to be expected given the reduced prices for many of the goods and services consumed by tourists, relatively weak growth in tourism numbers, and squeezed incomes in Europe and America due to the poor economic climate. There is a small improvement of €17m in the year following the introduction of the Jobs Initiative.

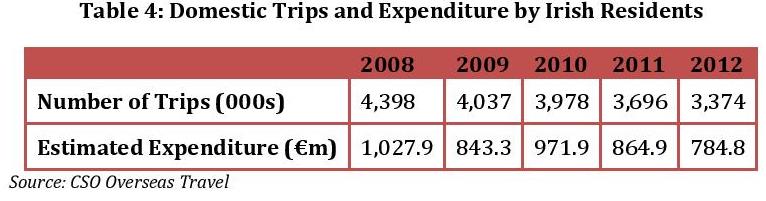

Domestic Holidays

Lower prices should in theory impact not just the decisions of overseas travellers, but should also change the decision of Irish residents with regards holidaying abroad or at home. Evidence from the Household Travel Survey, however, shows that the decline in domestic holidays by Irish residents since the peak of 2008 has continued unabated. Estimated expenditure by domestic holiday-makers shows a similar decline.

Comment on timing

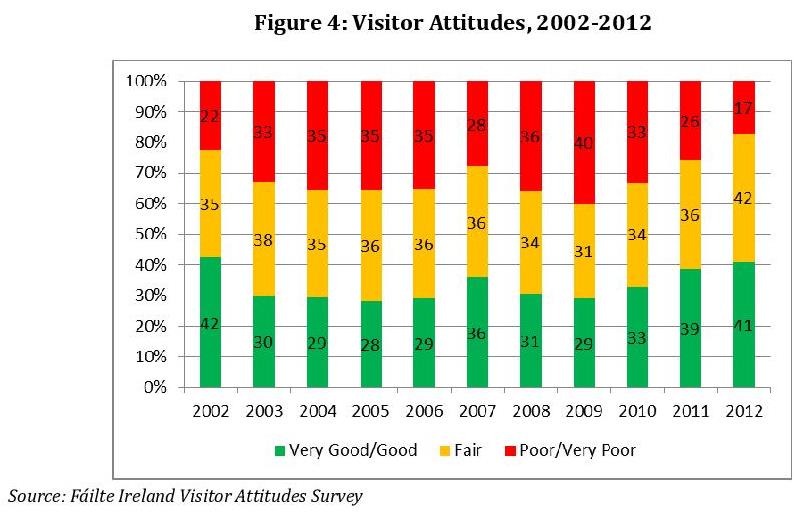

The analysis above seeks to determine whether or not there was a significant response from tourists to the 9% rate of VAT following its introduction in the second quarter of 2011. Implicit in this analysis is the assumption that any response would become apparent immediately following the policy change. There are reasons to believe this approach is reasonable: the internet allows prospective tourists to compare price and quality of accommodation, food services and attractions before they choose a destination to travel to. However, the policy change may also have a delayed impact via encouraging more visitors to return in the future or to recommend Ireland to a friend. Ireland has garnered a reputation as a high-cost holiday destination, and it may take some time to change perspectives.

Evidence from the Fáilte Ireland annual Visitor Attitudes Survey shows a marked improvement in perceptions with regards to Ireland’s value for money. The fraction of visitors rating Ireland’s value for money as poor or very poor is lower than it has been for over a decade. What role the VAT reduction had in improving perceptions of value for money – and the longer-term impact of this improvement on the tourism sector and the wider economy – is difficult to determine. The significant improvement over 2011/12 coincides with the weakening of the euro versus the dollar and the pound, which had a comparatively larger impact on the purchasing power of visitors from the US and the UK. However, the improvement in attitudes is also observed in surveys of visitors from France and Germany, who were not directly affected by the weakening of the euro.

2.Shifting the Burden of Taxation

The second goal of the lower rate of VAT was to shift the burden of taxation away from those industries that are labour-intensive. Unlike the goal of stimulating tourism, it is not necessarily important that businesses pass on the VAT rate reduction to customers. The only concern is whether or not the policy improved employment in the affected sectors.

Employment data

Unfortunately, jobs data is not available in sufficient detail to accurately determine the full policy impact. Data is available on employment in accommodation and food services, but not for other sectors such as printing, hairdressing and recreational services. This lack of data makes it difficult to evaluate the effectiveness of the policy without making some assumptions and conjectures. This has led to a wide range of estimates of the impact of the reduced rate of VAT, from 5,600 to 35,000 jobs created.

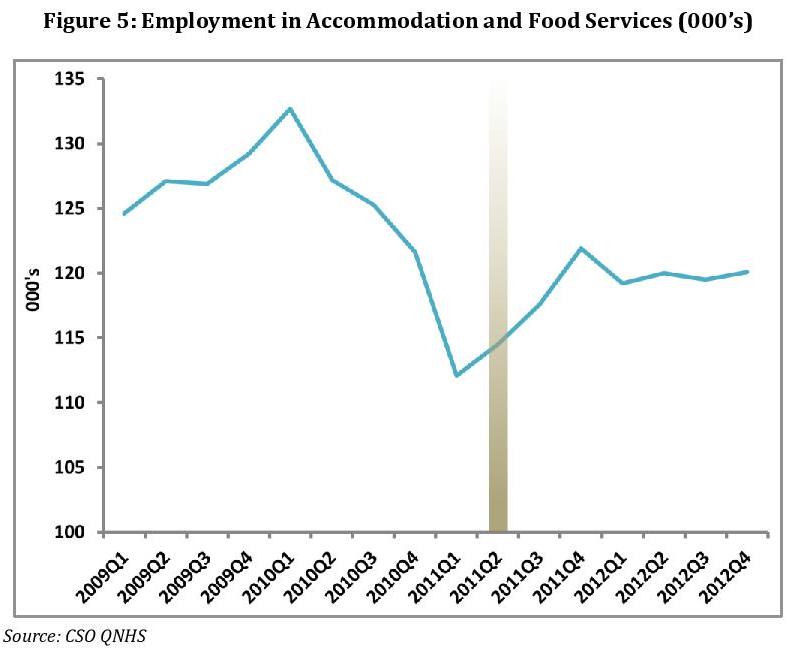

Although we do not know precisely how many people are employed in sectors that benefit from the 9% rate, accommodation and food services makes up 70% of the cost of the VAT reduction, so that we can use this sector as a reasonable proxy for the policy’s wider impact. The graph below charts employment in this sector since 2009 using quarterly numbers that have been corrected for seasonal variation. Over 20,000 jobs were lost between the beginning of 2010 and early 2011. A relatively muted recovery has been taking place since the second quarter of 2011, which had added 8,000 jobs by the end of 2012. 5,600 of these jobs were created after the introduction of the 9% rate.

This data mirrors what we saw with regards to tourism numbers: growth began before the Jobs Initiative was announced. While one quarter of growth does not in itself mean that a recovery was inevitable, it does imply that a continuation of job losses at the rate experienced in 2010 was unlikely.

Estimates of Employment Impact

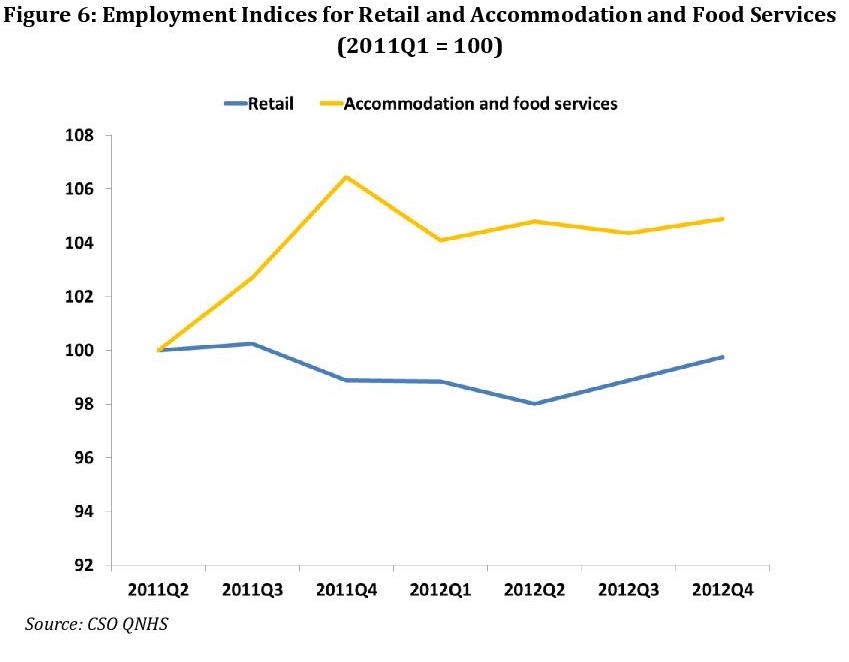

Saying that 5,600 jobs were created after the introduction of the 9% rate is not the same as saying that the policy led to the creation of 5,600 jobs. We encounter the same counterfactual problem that was observed when looking at tourism numbers: the alternative scenario where the policy was not enacted is not observed. However, we can compare employment in accommodation and food services with another similarly labour-intensive sector. The retail and wholesale sector is subject to many of the same economic forces as accommodation and food services; In particular, they both gained from the reduction in the rate of employer PRSI, another Jobs Initiative policy. One area in which the two sectors do significantly differ is that the retail sector is less likely to be directly affected by the weakening euro.

The graph below shows employment in both sectors indexed to the second quarter in 2011 (i.e. the period in which the policy was introduced). While employment in accommodation and food services improved in the 18 month period following the announcement of the Jobs Initiative, employment in retail did not fare as well, and ended the period roughly where it started. If employment in accommodation and food services had followed a similar pattern, employment in that sector would have been the same as in the second quarter of 2011.

Comparing employment in accommodation and food services to employment in retail is only one of several possible means of estimating the employment gain from the VAT cut. In an analysis carried out for Fáilte Ireland , Deloitte use as a comparator employment in all services excluding accommodation and food services, the public sector and the ITC sector , and find that employment in accommodation and food services was higher by 6,600 jobs than it otherwise would have been by the end of 2012.

IBEC construct another counterfactual by extending the average trend observed in the 18-month period before the rate cut, and then adjusting the trend using observed changes in overall private sector employment . Using this method, they suggest that 17,000 more people were employed in accommodation and food services than otherwise would have been the case.

The question of how to incorporate employment outside of the accommodation and food services sector has also been treated differently by those analysing the impact of the rate cut. The Irish Tourist Industry Confederation state in their budget submission that two-thirds of employment in tourism is accounted for by accommodation and food services, and, by applying a similar rate of jobs growth to the remaining one-third, they estimate that 9,000 jobs were created in the tourism industry as a whole.

Both Deloitte and IBEC note that 70% of the value of the rate cut was accounted for by lost revenues from accommodation and food services. By assuming that this sector also accounts for roughly 70% of the employment affected by the rate cut, and that the other 30% experienced similar rates of employment growth, they arrive at a total of 10,000 and 25,000 jobs respectively. IBEC go on further to estimate the number of jobs that were created indirectly via the employment multiplier , coming up with a final number of 35,000 jobs created.

In the absence of hard data, it is not possible to effectively disprove any given figure for the number of jobs created or retained due to the rate cut. The larger estimates rely on more assumptions, and with each assumption used the probability that a single point estimate represents the true policy impact is reduced. Furthermore, these assumptions tend to be logically weak, so that any conclusions drawn will also be correspondingly weak.

Cost Per Job

The key question is not whether or not jobs were created by the rate cut, but whether enough jobs were created to justify the cost. The Department of Finance estimate of the cost of lowering the VAT rate to 9% is €350 million.

Looking at the benefits of the policy, estimates range from 5,600 to 35,000 jobs retained or created as a result of the VAT cut – Minister of Finance Michael Noonan cited job creation of 15,000 new jobs in his Budget 2014 speech – but the credibility of any given point estimate is low; the void created by the lack of hard data has been filled by generally weak assumptions and supposition. Based on the Department of Finance figure of €350m, the cost per job created is €23,333. Using the wider interval of 5,600-35,000 jobs, the cost per job of the 9% rate of VAT lies somewhere between €10,000 and €62,500.

Notes:

1 Callaghan, N. and Tol, R. ‘UK Tourists, The Great Recession and Irish Tourism Policy’ ESRI Working Paper 412, 2011

2 O’Connor, B. ‘Measuring the impact of the Jobs Initiative: Was the VAT reduction passed on and were jobs created’, Medium-Term Fiscal Statement, Department of Finance, 2012

3 Deloitte, ‘Analysis of the Impact of the VAT Reduction on Irish Tourism & Tourism Employment’ July 2013

4 It appears that they used a proxy of the private sector using the sum of all sectors less public administration and defence, education, and health and social work activities. A more reliable measure of private sector employment is provided by the CSO’s Earnings, Hours and Employment Costs Survey. Although this data is not seasonally corrected, the trend is more positive in terms of employment growth than the trend suggested by the proxy.

5 The remaining service categories are therefore wholesale and retail, transportation and storage, finance, insurance and real estate activities, professional, scientific and technical activities, and administrative and support service activities.

6 IBEC Budget Submission 2014

7 Seemingly using the same proxy as the Deloitte study.

8 Using a study of the Scottish tourism sector in 2009 that indicated that every 100 tourism jobs support 40 other jobs indirectly..

Tagged with:

VAT

About author

Related Articles

-

-

Fiscal Devaluation

19 Apr 2012

79 Merrion Square, Dublin 2, Ireland

tel: 353 (1) 676 0414 | email: info@publicpolicy.ie

Company registration number: 504956

Privacy Policy | Chairman's Blog | Events | Video | Public Policy Documents | News Property Tax Ireland | Pension Reform Ireland | Water Charges Ireland