{kind=link}

Residential Property Prices 2007 – 2016

9 Mar 2016Key Point

The Central Bank restrictions on mortgage lending have moderated the rate of increase in house prices which are still substantially below the unsustainable peak levels reached in 2007.

Context

In January 2015, new more restrictive mortgage lending regulations were introduced by the Central Bank. Limits were imposed on loan-to-value (LTV) and loan-to-income (LTI) ratios. The rules which apply to first-time buyers include an LTV limit of 90% up to €220,000 and loan-to-income (LTI) limits of three and a half times gross annual income for those buying a principal dwelling home (PDH). Additional sums above this value are subjected to an LTV limit of 80 per cent. Also, non-first time buyers of a PDH can avail of an 80 per cent LTV limit. Banks have discretion to allow 15 per cent of new lending for PDH mortgages to exceed the LTV limits annually. The rules are stricter on buy-to-let (BTL) mortgages as the LTV limit is 70 per cent, and this can only be exceeded in 10 per cent of cases for all non-PDH lending. However, the LTI limits do not apply to BTL mortgages.

Effect of Restrictions

The new restrictions have dampened the housing market1 . In the three months up to January 2016, the number of mortgage approvals fell by 14.7% (14 % by value) on an annual basis2 .

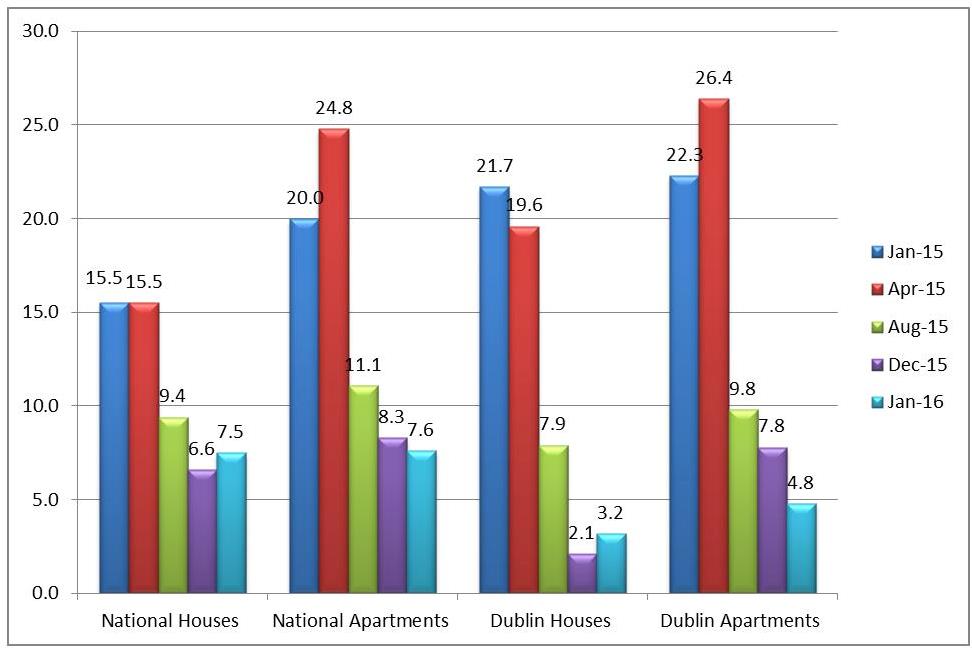

The rise in residential property prices has moderated particularly in Dublin. Figure 1 illustrates the year-on-year percentage change in prices between January 2015 and January 2016.

Figure 1 – Residential Property Prices – Percentage Change in 12 months

(Source: CSO)

Despite the rise in prices they are still substantially below peak levels which are now widely regarded as having been unsustainable. We examine the data below.

National – All Residential Properties

Property prices nationally peaked in 2007 and fell by 50.7% by March 2013. By January 2016, they had recovered by 35 per cent but are still one third (33.5%) below the peak reached in 2007.

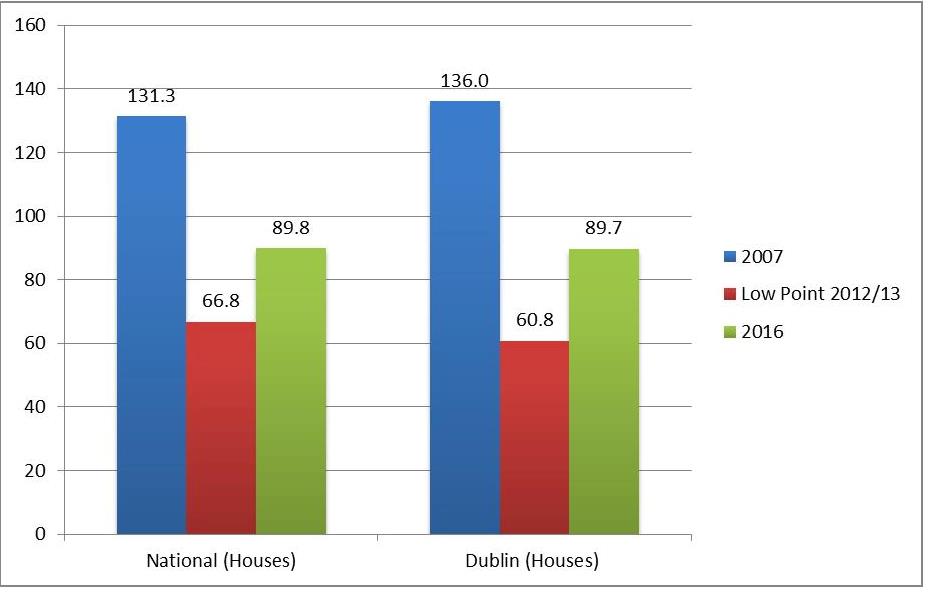

National Houses and Apartments

National house prices fell by 49 per cent up to March 2013 from their peak in 2007. As of January 2016, they were still 31 per cent below their peak.

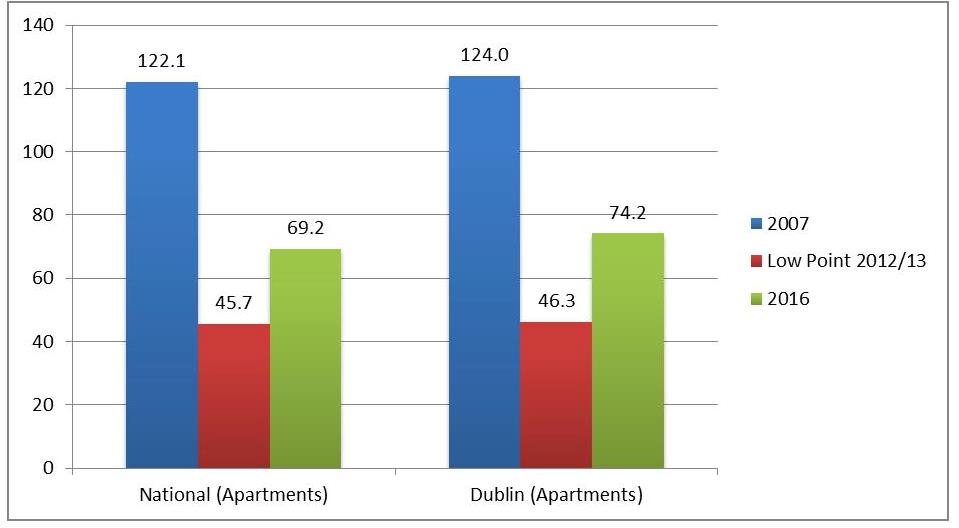

National apartment prices reached their lowest level in November 2012 decreasing by 63 per cent from their peak in 2007. By January 2016, they had recovered by 51 per cent but remain 43 per cent below their peak in 2007.

Dublin Houses and Apartments

Dublin house reached their lowest point in August 2012 falling by more than half (55.3%) since 2007. By January 2016, house prices recovered by 48 per cent but remain a third below (34%) their peak in 2007.

Dublin apartment prices fell by 62.7 % by November 2012 from 2007 levels. This is the highest percentage fall in residential property prices in a given sector. Prices have recovered (60.3%), but remain 40.2% below the peak prices achieved in 2007.

Figure 2 – House Prices Nationally and in Dublin

(Source: CSO) Base 2005 = 100

Figure 3 – Apartment Prices Nationally and in Dublin

(Source: CSO) Base 2005 = 100

________________________

Notes:

1 The key objective of these regulations is to increase the resilience of the banking and household sectors to the property market and to reduce the risk of bank credit and house price spirals from developing in the future. The Central Bank does not wish to regulate or directly control housing prices (Central Bank, 2015).

2 Banking & Payments Federation Ireland

Tagged with:

Property Tax

About author

Related Articles

-

-

Property Tax – Why Dubliners Should Pay More

19 Jan 2013

79 Merrion Square, Dublin 2, Ireland

tel: 353 (1) 676 0414 | email: info@publicpolicy.ie

Company registration number: 504956

Privacy Policy | Chairman's Blog | Events | Video | Public Policy Documents | News Property Tax Ireland | Pension Reform Ireland | Water Charges Ireland