{kind=link}

Low Income Self-Employed Are Unfairly Treated by the Tax System

25 Jul 2013Key Point

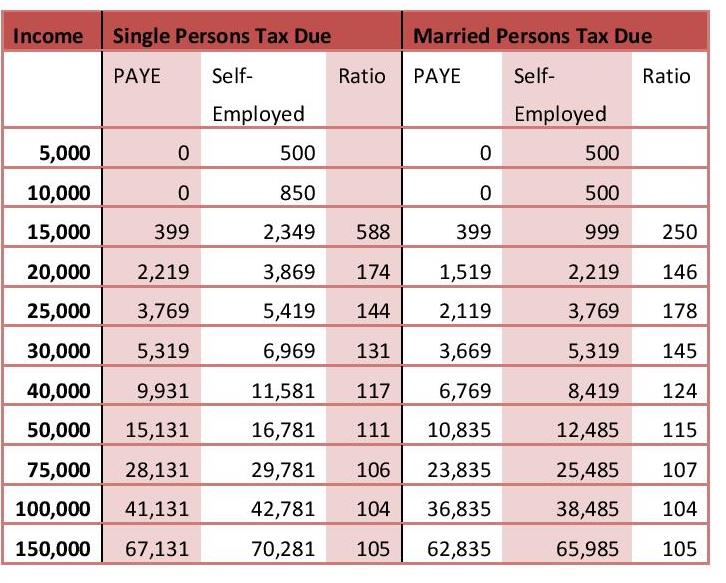

A self-employed single person on an income of €15,000 pays almost 6 times as much tax and PRSI as an employee on the same income.

Introduction

An important principle underlying the tax system is that of equity; in simple terms the amount of tax two people pay should be the same if their income is the same. In other words the source of your income should be irrelevant. The Irish tax system fails this basic test and the unfairness is particularly acute in the case of self-employed people on low incomes. The data is presented below.

Note: Tax includes Income tax, USC and PRSI

The Ratio Column is obtained by dividing the tax paid by the self-employed person by the amount paid by the employee and multiplying by 100. If the ratio is 100, they both pay the same tax. If it is more than 100 the self-employed person pays more.

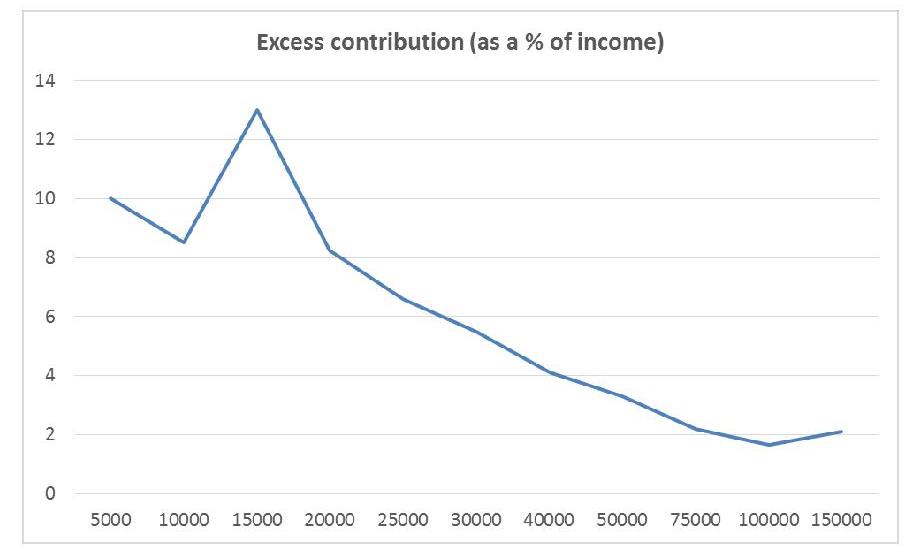

Excess tax paid by a single self-employed person (% of income)

Two factors explain the wide difference between the tax treatment of the self-employed vis a vis employees; the employee tax credit and minimum rates of PRSI.

The Employee Tax Credit

Employees are entitled to claim an additional tax credit (currently €1650). The credit is not available to amounts paid by a company to a proprietary director or to the spouse or civil partner of the person paying the income.

This allowance1 was introduced in the tax year 1980-81 at the rate of £400 (€508)2 . In introducing this allowance in the 1980 Budget, the Minister for Finance, Michael O’Kennedy said:

“I am providing a special Schedule Employee Allowance of £400 for each PAYE taxpayer in order to improve the tax progression for these taxpayers and also to take account of the fact that the self-employed generally have at present the advantage of paying tax on a previous year basis. I intend to exclude from this provision those Schedule E taxpayers in a position to control their own remuneration or that of their spouses, for example directors of proprietary companies. This Schedule E employee allowance is also intended to take account of the case made by ICTU that the present general scheme of allowances discriminates against employees and in favour of other taxpayers.”

Given the high rates of inflation at that time, the assessment of self-employed persons on their income of the preceding year conferred a significant advantage. This no longer applies as self-employed are now assessed on their current year’s income.

PRSI

Employees pay no PRSI if their income is under €352 per week. The self-employed pay 4 per cent of their income (with a minimum charge of €500). The self-employed also qualify for fewer benefits3 . They are entitled to Widowed Pension, State Pension, Maternity Benefit, Adoptive Benefit and Bereavement Grant. They do not qualify for other benefits such as Jobseekers, Illness, Dental and Optical Benefits.

Different rules for Deduction of Expenses

One possible justification for the higher taxes levied on self-employed taxpayers is that they have a more liberal expenses regime. For example, Minister Brendan Howlin said on the Marian Finucane Radio Show on 16 December, 2012 that the reason for the differential was that

“The self-employed have more tax deductible things they can claim”.

The expenses allowable for employees are limited to those “incurred wholly, exclusively and necessarily” in the performance of the duties of the office or employment. For self-employed the rules are different. Expenses incurred “wholly and exclusively for the purposes of the business” are allowed though there are restrictions on certain categories of expenses.

The reality is that the deductions allowed to self-employed individuals are ones that should be allowed in order to arrive at a proper definition of income under generally accepted accounting principles. Indeed, classes of expenses such as motor leasing and entertainment expenses which are restricted for tax purposes are fully deductible under accounting rules.

In addition the discrimination against self-employed taxpayers is regressive in that it is more extreme at the bottom of the income scale. If there were any validity in the more liberal expenses regime argument, the required adjustment would need to be very different.

Conclusion

There is a strong case for addressing the unfair treatment of self-employed particularly those on low incomes. A start should be made by reducing the amount of the Employee credit and increasing the personal tax credit which is available to all.

Notes:

With assistance from Donal de Buitléir

1 In 1980 tax reliefs were given in the form of allowances which were deducted from total income to arrive at taxable income. Rates of tax were then applied to taxable income to compute tax due. The value of the allowance varied with the marginal tax rate. A tax credit is deducted from the tax due and is of the same value to all taxpayers. A tax credit of €1,650 is the same as an allowance of €8,250 at the standard rate of tax.

2 Section 3 of Finance Act , 1980

3 There is an employer contribution paid on behalf of employees

Tagged with:

Self Employed

About author

Related Articles

79 Merrion Square, Dublin 2, Ireland

tel: 353 (1) 676 0414 | email: info@publicpolicy.ie

Company registration number: 504956

Privacy Policy | Chairman's Blog | Events | Video | Public Policy Documents | News Property Tax Ireland | Pension Reform Ireland | Water Charges Ireland