The Taxi Market In Ireland: To Regulate Or Deregulate?

23 Oct 2014Introduction

This note gives an overview of the economic issues surrounding regulation of the taxi market, a history of regulating the taxi market in Ireland, and an assessment of the 2010 reintroduction of a cap on taxi licences.

In 2010, following a decade of free competition in the taxi market, the government announced an indefinite prohibition on the issue of new taxi and hackney licences. This meant that entry to the market was restricted and this was largely in response to lobbying by the taxi industry and a perceived oversupply of taxis.

Recent research commissioned by the OECD to assess taxi regulation in Ireland has concluded that regulating the market by way of entry restriction is ill conceived and would lead to longer queues and waiting times for consumers1.

Summary of key conclusions:

- A number of market failures mean that the small public service vehicle (SPSV) sector is subject to government regulation in the form of price and quality control in order to protect the consumer.

- Taxis are part of the SPSV sector, which also includes hackneys, limousines, wheelchair accessible taxis (WAT) and wheelchair accessible hackneys (WAH).

- In December 2013, there were 17,136 standard taxis in Ireland, accounting for 78% of the SPSV market.

- Between 1978 and 2000, entry to the SPSV sector was restricted through quantitative limits on the number of licences issued. This meant that the sector, and particularly the taxi market, was undersupplied. This resulted in unfulfilled consumer demand, higher fares and longer waiting times.

- This restriction was lifted in 2000, and between 2000 and 2008, the number of taxi licences rose from 3,913 to 21,177, or 541%.

- In 2010, a restriction was re-imposed on the SPSV sector by way of an indefinite prohibition on issuance of new licences and a prohibition on trading of licences. This was largely unjustified and there is some evidence of regulatory capture.

- Given the current uptick in the Irish economy and expected improvements in domestic demand, the 2010 prohibition on issuing new licences should be lifted2.

The Economic Rationale for Regulating the Taxi Market

The SPSV market is one of many markets that receive some form of government intervention to protect consumers from a sub optimal outcome that could occur in the absence of such regulation. That is, there exists a market failure. A ‘sub optimal outcome’ could relate to excessively high prices, poor quality service, restricted supply, or price discrimination. Regulation surrounds taxi fares, driver/vehicle quality, fare control and market entry. The market for hackney (private hire) vehicles typically receives lighter regulation, where only driver and vehicle standards are subject to regulation.

While the market for taxis closely resembles a ‘textbook’ perfectly competitive market, a number of market failures mean that it does not achieve optimality in terms of the outcomes of a perfectly competitive market. For example,

- Lack of price information means that in the absence of fare control, consumers cannot tell whether the quoted fare is reasonable;

- Finding the taxi offering the best fare would be difficult and the consumer would likely incur considerable transactions costs in doing so (e.g. lost time);

- If consumers tried to find the best fare, this could cause congestion at ranks and on the road; and

- Consumers cannot determine the quality and safety of the taxi service in advance – e.g. the best fare could be in a less safe vehicle3.

These factors point toward the need for regulation of taxi fares and quality standards. For example, the European Conference of Ministers of Transport (ECMT) (2007) proposed a number of negative impacts from taxi deregulation which included suggestions that outright deregulation could lead to, amongst other things: chaos on streets, an increase in accidents, a decline in vehicle standards, and control of the sector by monopolistic dispatch centres.

Controlling entry

Free entry to the taxi market, as with any market, leads to lower prices, an adequate supply of the service, greater choice for consumers, greater service at peak times, and technical innovation on the part of service providers to boost their earnings.

However, there are three key motivations for controlling entry that frequent the economics literature: provision of low quality service, fear of congestion and overcrowding at ranks, and the cost of excessive entry.

Firstly, entry is controlled for fear that excessive entry will lead to an overall decline in the quality of service delivered. More intense competition could lead to drastic fare cutting behaviour and hence a decline in quality. In addition, free entry could encourage greater levels of part time work that could also reduce quality levels, and greater prevalence of ‘cream skimming.’ (Fingleton et al., 1998). As such, this is not an argument against deregulation of entry, but an argument for improved quality standards where entry is deregulated.

Secondly, regulation of entry can reduce traffic congestion and overcrowding at ranks. Vast numbers of taxis can impose a cost to society in the form of greater congestion on the road for all road users. External costs arise where the supply of cab services gives rise to costs to society as a whole (typically congestion, environmental costs, and road safety impacts) for which suppliers are not charged.

A third, albeit weak, argument for entry control relates to instances in which excessive entry or ‘churning’ (where there is constant entry and exit) can produce losses to the entrants and possibly push out already established (‘incumbent’) providers, while discouraging future entrants.

In countries with entry restrictions, the OECD reports that taxi numbers tend to remain constant or decline on a per capita basis, excess demand becomes evident and licences or plates become particularly valuable. The OECD remarks that the significant entry after deregulation in some countries is evidence of overly restrictive entry in the period prior to deregulation, particularly in Ireland and New Zealand4. The OECD favours free entry but strict quality regulation to ensure high vehicle and driver standards5.

A further issue with controlling entry is the difficulty of quantifying the costs and benefits – the costs of congestion, churning and the extent of lost income to providers, and the benefits to consumers of greater entry. Trying to match supply with demand accurately would be a tedious exercise (what is the required number of taxis in Dublin today?).

Academic Literature

There is a sizeable academic literature on the issues surrounding regulation of the taxi market, and this extends back nearly fifty years. Many studies show that long periods of regulation breed negative effects in the form of rent production (where taxis reap high profits), high licence value (allowing owners of licences to trade and achieve a capital gain on their investment), lack of response to increasing demand, collusive behaviour, longer waiting times and low quality service6. This apparent failure of the regulatory system in many jurisdictions is partially attributed to the ability of taxi operators to lobby and the consequential issues of regulatory capture7. Beesley and Glaister (1983) conclude that there is no public interest in restricting entry to the taxi market and that such restrictions can lead to detrimental outcomes and sub optimal supply8.

The Small Public Service Vehicle (SPSV) Sector in Ireland

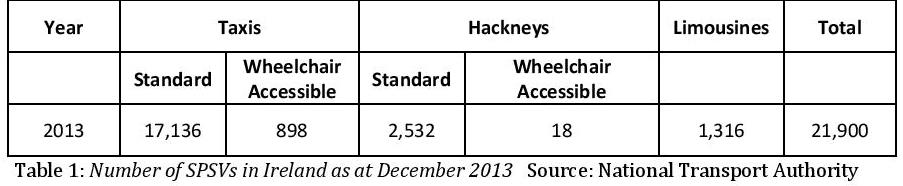

Taxis are part of the broader small public service vehicle (SPSV) sector, which refers to vehicles for public hire carrying up to eight passengers. The SPSV sector also includes wheelchair accessible taxis (WAT), hackneys, wheelchair accessible hackneys (WAH) and limousines9. The key difference between taxis and hackneys and limousines is that taxis can ply for hire on the street or in taxi ranks, and be pre booked for call out, whereas hackneys and limousines can only be privately booked and the fare is agreed in advance. Unlike hackneys, taxis are subject to maximum fare regulation. The table below gives a snapshot of the number of SPSVs in Ireland as at December 201310. There were 17,136 standard taxis in Ireland, accounting for 78% of the SPSV market. Limousines, which became a separate SPSV category in 2000, only account for 6% of the sector.

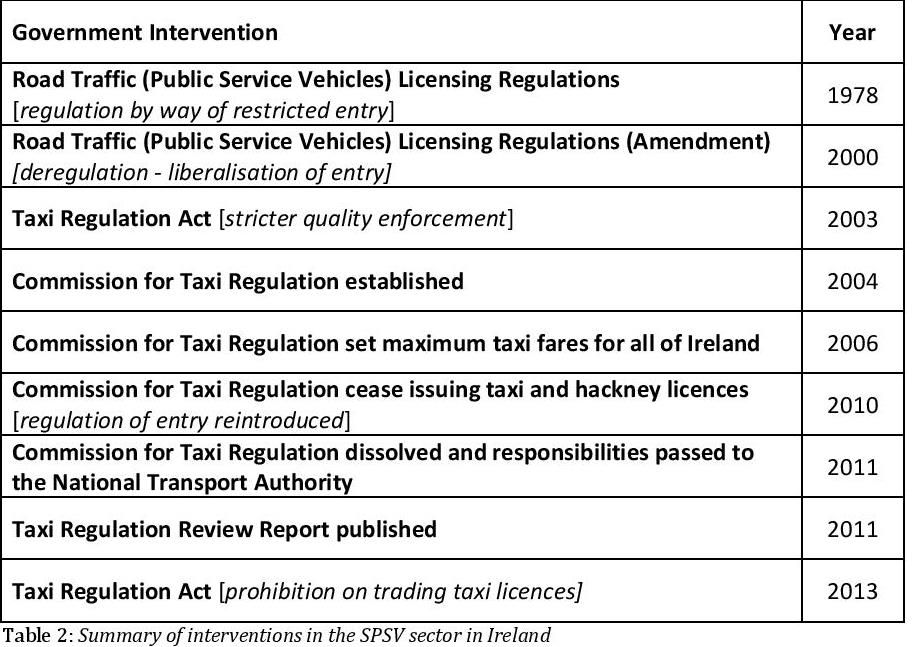

Table 2 gives a summary of the government interventions in the taxi market in Ireland since 1978.

During the period 1978 to 2000, entry to the taxi market in Ireland was restricted by way of a limit on the number of taxi licences issued. During this period, there was a small increase in the maximum number of licences for various reasons, e.g. demographic changes. Fingleton, Evans and Hogan (1998) present evidence to suggest that in 1998 there were not enough taxis to fulfil the demand for journeys in Dublin, and that a near equilibrium required 4,500 new licences at the time.

In 2000, this limit was repealed, removing any restriction on market entry. The removal of the limit on the number of licences arose out of criticism of the effects of regulation on the consumer and meant that any suitably qualified person could obtain a taxi licence. Following the removal of restrictions on the issuance of new licences in 2000, the number of licences in Dublin rose to 8,609 by 2002 with large increases in other parts of the country. Between 2000 and 2008, the number of taxi licences rose from 3,913 to 21,177, or 541% 11. This in itself is evidence of undersupply in the pre deregulation era.

The Commission for Taxi Regulation was set up in 2004, taking on the role that local authorities had previously taken, and became the National Transport Authority (NTA) in 2011. The NTA is responsible for licensing vehicles, while An Garda Síochána is the licensing authority for SPSV driver licences and sets out the SPSV driver licensing conditions. As part of the annual vehicle licensing process, vehicles are inspected for SPSV suitability, NCT certification is checked, and current tax clearance certificates are verified as mandatory requirements.

In 2010, limits on licence issuance were reinstated which meant that issuing new taxi and hackney (but not WAT, WAH or limousines) licences were prohibited, and subsequently in 2013, the trading of licences was prohibited.

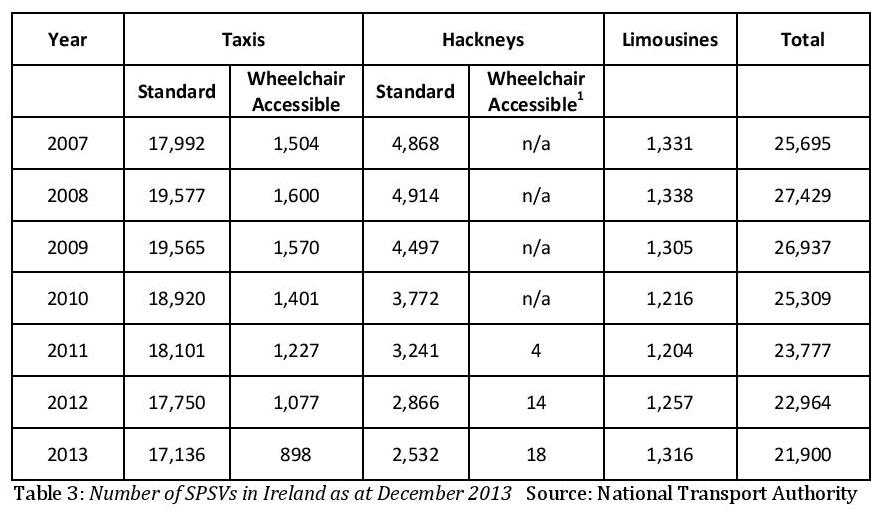

We see from the table below, that there has been a considerable decrease in the total number of taxis since 2010, with little or no change in the number of limousines. The total number of taxis (incorporating standard and wheelchair accessible taxis) declined by 14.8% between 2008 and 2013. This illustrates the sizeable exit from the market.

* Wheelchair Accessible Hackneys (WAH) were introduced in 2010

Why was entry to the taxi market re-regulated in 2010?

Broadly speaking, the decision to re-regulate entry surrounded the onset of the recession in Ireland from 2008 onwards. This led to a reduction in demand for taxi services, fare discounting, reduced incomes among taxi drivers, and a wedge between the demand and supply of taxis.

The two key arguments for the 2010 policy relate to (1) the perception of oversupply of taxis and (2) concerns that the market was not providing sufficient services to wheelchair customers.

1. The indefinite prohibition was put in place to curtail entry to the market to restore the supply/demand balance. Independent economic analysis published in the Taxi Regulation Review report (2011) showed that the fall in demand after the economic downturn was not matched by corresponding exit from the sector and hence an oversupply of SPSV services existed. National oversupply was estimated to be in the range of 13-22%. While fares in Ireland were found to be above other countries, they were broadly similar to what would be expected given wages, employment and population density. Policymakers were advised to ensure that there was no disincentive from exiting the market. Gorecki (2014) argues that, if oversupply is approximately 22% per annum, this should be eliminated by 2015-2017 and that there is no need for an indefinite prohibition on licence issuance.

2. The 2010 prohibition on new licences does not pertain to WAV or WAH licences. For example, in 2013, WAT only accounted for 5% of the total number of taxis (WAT and standard), and WAH accounted for less than 1% of total hackneys (WAH and standard). The Commission for Taxi Regulation’s Regulatory Impact Assessment of the sector in 2009 argued for a target for wheelchair accessible vehicles of 10% of the overall cab fleet. This target or any associated timetable was not included in the 2010 prohibition. Gorecki (2013, 2014) asserts that given the higher costs of running a wheelchair accessible vehicle, there is unlikely to be increased entry into this segment of the market and this is consistent with the figures in table 3 above. Indeed, the Taxi Hardship Panel, set up in 2002 after the 2000 deregulation, received a large number of hardship claims under the category ‘WAT Operators Claiming Higher Operating Costs.’

Regulatory capture

The Goodbody (2009) report of the SPSV sector found that there was no need for a moratorium on the issuance of new licences, and pointed out the likely adverse effects of said moratorium on consumers. Goodbody and the Commission for Taxi Regulation appeared before a Joint Oireachtas Committee on Transport in March 2009 and the Goodbody report was challenged in terms of conclusions and methodology. The Committee called for a three year moratorium on licence issuance and felt that such a moratorium would deliver ‘a higher quality, more efficient and superior service.’

This represents a clear rejection of expert economic analysis and could be seen as an example of regulatory capture.

The Impact of Government Interventions in the Taxi Market

In a recent report commissioned by the OECD on the competitive effects of government regulation in Ireland, Gorecki (2014) assesses government intervention in the taxi market in Ireland over the period 1978 to 2014.

Among the indicators employed by Gorecki (2014) to assess the impact of regulation include the number of licences (i.e. the number of taxi service providers and hence the impact of restricted entry), the degree of substitutability between taxis and other small public service vehicles, the value of taxi licences, and fare discounting and waiting times.

Number of licences

The impact of licence restriction is considered effective if its removal leads to an increase in supply. There was a marked increase in taxi operators in Ireland post 2000: by 2002, there were substantial increases in taxis: in Dublin from 2,722 to 8,609; in Cork, 216 to 590; and, in Waterford, 41 to 147.

Substitution

When there is a cap on the issuance of new taxi and hackney licences, is it the case that WAT, WAH or limousines can fulfil any excess demand? The 2010 prohibition does not apply to WAT, WAH or limousine licences but given the uncertainty of the duration of the 2010 prohibition, we are unlikely to see large entry into the WAT, WAH and limousine markets.

WATs and WAHs, given their high costs of operation 12 , are likely to be substitutes for taxis only when quantitative controls on taxis create a sufficient rent to induce WATs to offer regular taxi services. In light of these higher costs and the practice of current price discounting by SPSVs, additional WAT/WAH are unlikely to enter the market and substitute for regular taxis until there are substantial returns to compensate for such higher costs. This is consistent with the data; from Table 3, we see that the number of WATs has declined since 2008.

When the economy recovers more widely and demand for SPSVs picks up, we are then likely to see a rise in the number of WAHs and WATs, many of which may serve non wheelchair users since the returns to servicing these users is likely to be higher – both due to overall higher demand and the cap on issuance of new taxi licences.

Taxi licence values

As the value of a taxi licence is likely to increase as demand for taxi services increases (and vice versa), the market value of a licence is a good indicator of the level of over- or under-supply in the market. In 2010, the quantitative limits on issuance of new licences also prohibited the transfer of taxi licences, allowing them to only be transferred one more time and to a vehicle that was less than three years old. In this way, licence values can no longer be an indicator of the level of over- or under-supply in the market relative to demand.

Between 1978 and 2000, taxi licence values rose tenfold over this period as demand for taxi services increased and there was no commensurate increase in the supply of taxis as a result of the cap on new licences. After 2000, the value of licences plummeted when entry to the market expanded, and the Taxi Hardship Panel was unable to compensate taxi licence holders for the loss in the capital value of their licence.

By prohibiting tradability of licences, it is likely that the NTA will face a number of stakeholders lobbying for a change in legislation because as the value of licences rises, owners of a licence will wish to realise that value.

Gorecki (2013) notes also that prohibiting the transfer of licences may limit flexibility in the market as being unable to sell a licence could prevent exit from the market.

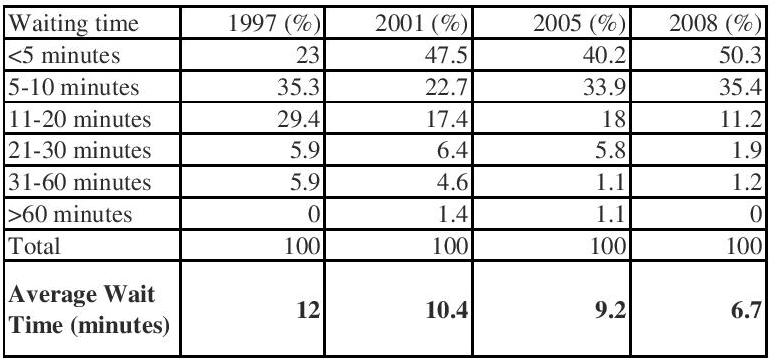

Waiting times and fares

Table 4: Dublin Waiting Times 1997 – 2008 Source: Goodbody (2009, p.49)

As illustrated in Table 4, the Goodbody (2009) surveys of consumers showed that average waiting times for cabs fell between 1997 and 2008. In 1997, the average waiting time was 12 minutes, which fell to 6.7 minutes in 2008, representing a saving of 5.3 minutes.

Goodbody (2009) note that the liberalisation of entry reduced consumer waiting times – they estimate consumer benefits of between €284 million and €313 million due to shorter waiting times in Dublin (€780 million nationally) over the period 2000-2008 (table above), based on specified estimates of the value of time. In Dublin in 1997, 77% of passengers waited more than 5 minutes for a taxi, but following the removal of the cap on taxi numbers, the corresponding percentage in 2001 in Dublin was 52.5%. However, broadly speaking, waiting times have not fallen by very much.

With regard to fares, Gorecki (2014) finds that fares have generally fallen in response to declines in demand brought about by the recession. In 2012, more than 75% of taxi drivers and 83% of dispatch operators offered discounts to customers. Gorecki concludes that notwithstanding some excess capacity, the market appears to be adjusting well to falling demand since 2008 with price discounting and a number of exits from the market.

Conclusions

The substantial increase in supply of taxis in the aftermath of the 2000 liberalisation of the market lends support to the notion that the market was undersupplied between 1978 and 2000. Goodbody (2009) and Gorecki (2014) show that customer-waiting times fell, prices declined and the value of taxi licences decreased – an important indicator of the demand/supply balance.

However, with the onset of recession from 2008 onwards, there were a considerable number of exits from the market but this was not sufficient to meet the decline in demand, and it was perceived that the market was still over-supplied.

In 2010, an indefinite prohibition was introduced which prohibits the issuance of new licences and the trading of current licences.

Given the current uptick in the Irish economy , it can be expected that demand for taxi services is likely to increase and this, along with the negative effects of entry restrictions to the taxi market, is sufficient grounds for removing the 2010 prohibition.

The removal of the indefinite prohibition on the issuance of new licences could generate an expansion of entry into the market, and if coupled with strict quality controls, this could ensure that consumers are delivered a high quality service with low waiting times and the lowest fares.

References

Barrett, S. (2003) ‘Regulatory Capture, Property Rights and Taxi Deregulation: A Case Study’ Economic Affairs vol. 23, 4, 34-40

Beesley, M. and Glaister S. (1983), ‘Information for Regulating: The Case of Taxis’ The Economic Journal, vol. 93, 594-615

The European Conference of Ministers of Transport (ECMT) (2007) (De)regulation of the Taxi Industry Round Table 133, OECD/ECMT http://internationaltransportforum.org/pub/pdf/07RT133.pdf

Fingleton, J., Evans, J. and O. Hogan (1998) ‘The Dublin Taxi Market: Re-regulate or Staying Queuing’ Studies in Public Policy, Policy Institute, Trinity College Dublin https://www.tcd.ie/policy-institute/assets/pdf/BP3_Fingleton_Taxis.pdf

Frankena, M. W. and Pautler, P. A. (1986) ‘Taxicab Regulation: an Economic Analysis’ Research in Law and Economics vol. 9, 129–165

Gallick, E. C. and Sisk. E.D. (1987) ‘A Reconsideration of Taxi Regulation’ Journal of Law, Economics & Organization vol. 3, 1, 117-128

Goodbody Economic Consultants (2014) ‘Economic Review of the Small Public Service Vehicle Industry’ http://www.nationaltransport.ie/downloads/taxi-reg/economic-review-spsv-industry.pdf

Gorecki, P. (2014) ‘Evaluation of Competitive Impacts of Government Interventions’ OECD Working Party No. 2 on Competition and Regulation, DAF/COMP/WP2(2014)6, http://www.oecd.org/officialdocuments/publicdisplaydocumentpdf/?cote=DAF/COMP/WP2(2014)6&docLanguage=En

Gorecki, P. (2013) ‘The Small Public Service Vehicle Market in Ireland: Regulation and the Recession’ Economic and Social Review 44, 2, 247-272.

Gorecki, P. (2009) ‘The Recession, Budgets, Competition and Regulation: Should the State Supply Bespoke Protection?’ in T. Callan (ed.) Budget Perspectives 2010, Research Series No. 12, pp. 19-53. Dublin: Economic and Social Research Institute.

Heyes, A. and Liston-Heyes, C. (2007) ‘Regulation of the Taxi Industry: Some Economic Background’ in (De)regulation of the Taxi Industry Round Table 133, OECD/ECMT http://internationaltransportforum.org/pub/pdf/07RT133.pdf

Kahn, A. (1975) The Economics of Regulation Vol. 2, New York: Wiley & Sons Inc.

Kang, C. (1998) ‘Taxi Deregulation: An International Comparison’ Technical Report, International Transport Workers’ Federation, London http://www.taxi-l.org/kang0898.htm

OECD (2007) ‘Taxi Services: Competition and Regulation’ Policy Roundtable http://www.oecd.org/regreform/sectors/41472612.pdf

Radbone, I. (1998) ‘Looking at Adelaide’s Taxi Industry’ Road and Transport

Research vol. 7, 2, 52-59

Rometsch, S. and Wolfstetter E. (1993) ‘The Taxicab Market: An Elementary Model’ Journal of Institutional and Theoretical Economics vol. 149, 3, 531-546

Taxi Regulation Review Report (2011) Report of the Review Group, December 2011 http://transport.ie/sites/default/files/node/add/content-publication/Government%20Report%20on%20Future%20of%20Taxi%20regulation.pdf

Toner, J. (1996) ‘English Experience of Deregulation of the Taxi Industry’ Transportation Review vol. 16,1, 79-94

Viscusi, K., Vernon, J. and Harrington, J. (1996) Economics of Regulation and Antitrust, Second Edition, Cambridge, MA: MIT Press

Williams, D.J. (1980) ‘The Economic Reason for Price and Entry Regulation of Taxicabs: A Comment’ Journal of Transport Economics and Policy, vol. 14, 105-112

Notes:

1 Gorecki (2014)

2 The Economic and Social Research Institute forecast 5.2% economic growth in 2015.

3 Goodbody (2009)

4 OECD (2007)

5 Ibib

6 Williams (1980); Beesley and Glaister (1983); Frankena and Pautler (1986); Gallick and Sisk (1987); Rometsch and Wolfstetter (1993); Barrett (2003); Toner (1996); Kang (1998); Fingleton et al. (1998); Radbone (1998)

7 Viscusi et al. (1996); Kahn, (1975)

8 This is also the stance of the Competition Authority:

9 http://www.citizensinformation.ie/en/travel_and_recreation/public_transport/regulation_of_taxis_and_small_public_service_vehicles.html

10National Transport Authority, Taxi Statistics for Ireland March 2014

11 Gorecki (2014). Gorecki (2013) notes that part of this increase in licences may have been attributable to hackneys switching to be a taxi

12 Gorecki (2013) provides details on the costs of wheelchair accessible taxis, p. 256.

nbsp;.

{kind=link}

About author

79 Merrion Square, Dublin 2, Ireland

tel: 353 (1) 676 0414 | email: info@publicpolicy.ie

Company registration number: 504956

Privacy Policy | Chairman's Blog | Events | Video | Public Policy Documents | News Property Tax Ireland | Pension Reform Ireland | Water Charges Ireland