It Is the Right Decision Not To Sell Coillte’s Timber Harvesting Rights.

24 Jun 2013Key Point

The Government has decided not to sell the harvesting rights to the State owned forests managed by Coillte. This is the right decision.

A sale would have yielded a substantial lump sum, probably in the order of €700 million. The amount would depend on wood prices, discount rates and conditions imposed. The financial costs of securing this lump sum would comprise the foregoing of the future flow of income which these forests generate, which at present is used mainly to pay for costs (replanting, road building, amenity and recreation provision, pension costs etc.). These costs would continue to be incurred after the sale; they have a present value in the order of €500 million.

In addition to the financial considerations, there are two aspects which complicate the analysis:

- The first is the incumbent forest products industry, which depends on the flow of wood from Coillte, which supplies over 85% of the wood. Periodically, sealed tenders are sought, and the wood goes to those who bid the highest price. In the event of sale of the harvesting rights, a new owner (who would have close to monopoly power in terms of wood supply) might decide to depart from sealed bid auction sales and limit supply to one mill or a few mills. Over time, this could result in a very dynamic forest products sector, but there would be significant transitional costs.

- The second is the amenity value for recreation. Coillte facilitates and encourages access by the public. Compared to many developed countries, Ireland has a poor endowment of publicly owned forests and national parks. For most in Ireland, Coillte is the only forest recreation game in town; limitations on access could impose substantial losses. A new owner might well decide to facilitate and encourage visitors, but might not. In addition, there are the usual challenges that can occur with an ownership transfer, where financial stresses could result in harvesting more than the sustainable yield, and pose difficulties for meeting environmental and related commitments and conditions.

Given these complications, and the magnitude of the financial yield expected, I conclude that the decision to retain the harvesting rights in public ownership is correct.

However, the evidence base could be substantially improved, independent expert analyses of performance (financial, silvicultural, environmental, amenity and recreation etc.) should be publicly available; there is a case for allowing a new entrant to take over a substantial area – perhaps 30 thousand hectares – and innovate in terms of costs, products and services.

Introduction

Keynes observed:

Each age needs to distinguish for itself between what the state ought to do, and what ought to be left to the individual, or, in Bentham’s term, between the Agenda and the Non-Agenda of government.

In Ireland, we are at present being required to decide on the agenda and non-agenda of government in a variety of spheres. As regards assets and associated activities, there are at least four forms of state intervention: wholly owned, partially owned, privately owned but shaped by regulation, and privately owned untrammeled by regulation.

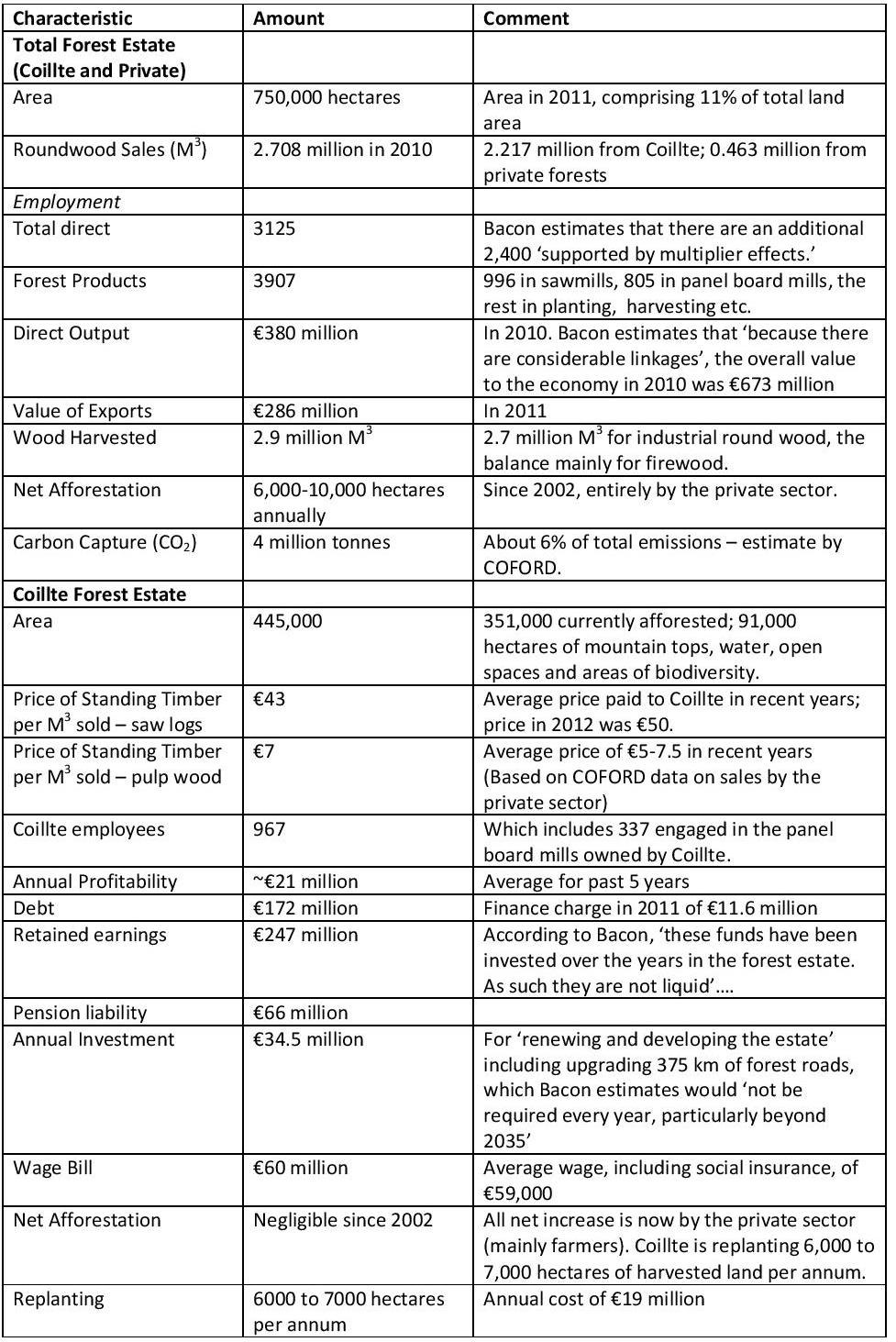

Coillte is a state owned company which since its foundation in 1988 manages Ireland’s national forests. All of the shares in the company are held by the Minister for Agriculture Food and the Marine and the Minister for Finance on behalf of the Irish State. These forests were created in part from the woodland ‘left over’ after the large estates were distributed to the former tenants, but mainly from the buying of land and its planting by the State. This creation of new forests commenced in the 1920s, and continued up to the late 1990s. It took place almost exclusively on land with little or no value for agriculture, and was motivated in part by a national desire to re-create the forests of the past when wood was plentiful and Ireland was free. The restoration of our woodlands had similarities with the restoration of the Irish language – a national project to restore that which was lost. As State planting wound down, there was a corresponding increase in private planting, which gathered momentum through the 1980s and 1990s, with a peak reached in 2001 when more than 15,000 hectares were planted; the private afforestation rate has since fallen, amounting to around 6,000-7,000 hectares annually over the past 5 year1.

The State planting policy was driven by two simple imperatives – don’t compete with farming, and plant a certain specified area per year, with the annual area planted ranging from time to time from 4,000 to 10,000 hectares and more. An irony of these policies was that most of the land purchased was too poor to support commercial crops of indigenous species. Instead of re-creating the forests of a mythic Celtic past, plantations of Sitka Spruce and Lodgepole Pine (Pinus Contorta) from the Pacific North West of North America became the new norm in the Irish uplands. Because the return on investment in forestry for wood production generally increases the better the land, the commercial returns on investment were substantially lower than would have been yielded with the purchase and planting of more fertile land.

When considering this form of privatisation, the following are the inter-linked considerations that should shape the decision:

- Is there government failure, in the sense that the asset is being managed by the State inefficiently (higher costs and/or poorer service than would be delivered by the private sector)?

- Is more competition likely to be the outcome of privatisation?

- Is there likely to be market failure, ie. are there substantial non market benefits that will be foregone, or external costs imposed, by privatisation?

- Will the sale generate substantial net revenues, that will make the transaction and other costs of the sale worthwhile?

These issues are addressed below. Notes are provided at the end of this commentary giving more detail and sources on area planted, finance, recreation valuation, and general facts, the latter drawn mainly from a report by Bacon and Associates on the issue commissioned by Impact, a trade union which represents many of the employees of Coillte.

Inefficient Management?

Coillte’s annual report for 2011 shows fixed assets valued at €1,469 million, and profits after tax of €20 million, a financial rate of return on fixed assets of 1.3% which is very low. However, if we add to this the annual value of recreation (18 million visits) estimated by Mayor, Scott and Tol of the ESRI at €77 million (see Note 2 for the detail on this estimate) – the rate of return on fixed assets increases to a more respectable 6.6%. Peter Bacon and Associates3 observe that the privatisation of the State owned plantation forests (1.8 million hectares) of New Zealand reduced costs and increased innovation, but they add that Coillte has benchmarked itself against best practise, improved productivity over time – doing more with less staff – and this is likely to continue.

More Competition?

There are large economies of scale and scope in the forest enterprise, and therefore there is likely to be some sacrifice in efficiency if the estate were broken up. Coillte contributes 87% of total round wood sales, and a much higher proportion of sales to the forest products industry. If it were sold as a block, a private monopoly would replace a State monopoly, although this market power would weaken over time as the more recent planting on private land begins to add to the flow of wood coming to market.

Market Failure?

The State enterprise produces two important benefits that could be compromised by a State sale. The first is the sustainability of the local timber processing sector (sawmilling and panel production).

Coillte is the almost exclusive source of round wood for this industry (the private forests are too young to yet deliver much commercial wood). It sells the wood by sealed big auction, and commits to put a specified volume up for sale each year. The forest products industry employs about 4,000, has a direct output value of €380 million (which Bacon Associates estimates can be doubled ‘because there are considerable linkages’), and annual exports amount to €286 million.

There is no guarantee that new owners would want to continue to guarantee to sell a specified volume by auction (which gives every processor the opportunity to bid and secure his or her supplies). They might wish to build their own plant and supply most of the wood to it, and/or to export round wood, or some combination, and this could result in a more dynamic forest processing sector.

It is conceivable that the existing processors could make up a roundwood supply deficit by imports – and wood prices in Ireland generally exceed those achieved in the UK – but they are located inland near the Irish forests, which are not near the coasts, and so the costs of transport would likely be prohibitive. Also, there may be phyto-sanitary risks (disease importation) arising, which could probably be overcome, but at a considerable cost in terms of inspection and testing. A sense of the very demanding requirements in place can be judged from the Forestry Commission’s regulations relating to Great Britain4.

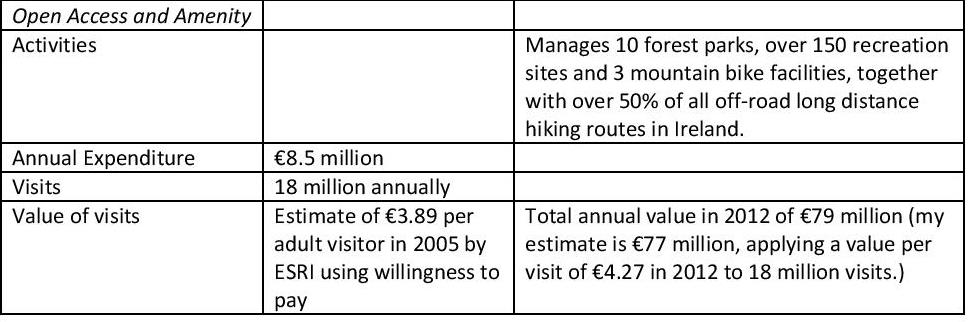

Coillte operates an ‘open forest’ policy, where any and all many enter, and also manages 10 forest parks, over 150 recreation sites and 3 mountain bike facilities, together with over 50% of all off-road long distance hiking routes in Ireland. There are about 18 million visits annually, valued (there is no entry charge), at about €77 million. It is possible that a private owner would continue to operate the open forest policy, and provide related services.

Substantial Revenues?

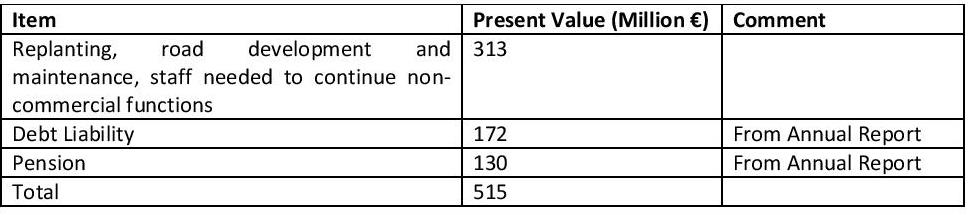

Applying a discount rate of 8% to the expected stream of wood sales, Bacon and Associates argue (p. 34) that “potential purchasers are likely to base their bids on recent timber prices, which are €43.10 if averaged over 5 years or €50 if 2012 is used. If we take the mid-point of this range then this provides a central estimate that the sale will realise €774 million.” But they note that the State would have legacy financial costs now being met from Coillte’s cash flow which would have to continue to be paid with or without the sale (Table 1)

Table 1. Estimate Of Financial Costs That Will Continue After Sale

If these continuing financial obligations are netted out of the present value of net revenues of €774 million, this yields a net of €259 million. And this turns out not to be far off the Bacon valuation of the company sold as a going concern. Bacon and Associates note (p.44) that:

“Coillte’s Annual Report 2011 shows an operating profit of €32.4 million and profit after taxation of just under €20 million. This was just below the 5 year average profit of €21.125 million. Applying a P/E of 10 to the 2011 profit would provide a valuation of €200 million.”

When Bacon and Associates add the present value of Coillte’s stream of revenues foregone – estimated at €565 million5 – to the above costs, together with a value for loss of amenity (estimated at €105 million), and the value of Coillte job losses (estimated at €19 million), they find that selling would result in a substantial net loss.

Discussion

The sale of harvesting rights would likely yield over €700 million6 , but would mean that the stream of annual revenues which Coillte generates at present, which is used to finance road building, re-planting, provision of amenity services, pensions etc., would be foregone. Capitalising future income into a lump sum available now is of course the point of privatisation; the choice comes down to how important we judge a lump sum now versus a future income stream.

If Coillte were sold as a going concern, with a requirement to maintain its recreation, amenity and other services, its financial value would probably fall in the range of €200-300 million.

The value of its recreation services is estimated to be about €77 million annually. The utility of such access is likely to be especially valuable for those whose incomes are very low; it represents a form of freedom, at a time when other freedoms are shrinking. But these recreation values do not translate into cash – access by the public is free. And the estimates of visit numbers (18 million), and the estimates by Mayor Scott and Tol (ESRI) of value per visit are both in need of updating (the valuation is based on a survey of over 1,200 households undertaken in 1998).

An export oriented forest products (saw logs and panels) business employing about 4,000 in rural areas has developed. These firms buy saw logs by sealed bid auction from Coillte, which supplies over 85% of the market. The volume of logs to be sold annually is guaranteed, but who gets them depends on who pays the highest price. Companies expand, contract or go out of business in part on the extent to which they compete successfully or not for the supply of logs. The purchaser of the harvesting rights could decide to continue supplying by sealed tender, and/or favour one or more processors which they might own. The latter procedure could sustain a large integrated plant which has economies of scale and scope, and can innovate and develop and secure new markets. But at the cost of contraction or closure of some existing plants that are at present commercially viable.

Would there be an efficiency gain from transfer of ownership? While the monopoly power of the purchaser would weaken over time as the supply of logs from private forests increases, for a decade or more they would be the dominant supplier of wood to the Irish market. Private monopolies are not necessarily more efficient than their public counterparts. Peter Bacon and Associates note that “Coillte has undertaken several rationalisation programmes since its establishment in 1988 including benchmarking against best international practice. Furthermore, the organisation outsources much of its forestry operations including harvesting and replanting”. Nevertheless, there might well be some efficiency dividend from introducing new people, management systems and techniques and innovations.

As regards amenity and recreation, Coillte provides services that are valuable, although the data on the magnitude of use and value needs updating. Would these continue to be provided in the event that the harvesting rights were sold? There are positive precedents from other countries, e.g. Scandinavia, where access is provided for the public to privately owned forest land. In others, access is provided under certain conditions. But in all cases, the public also have access to extensive areas of publicly owned – national, State and local – forest and parkland, in addition to the usual regional and urban parks. In New Zealand, 99% of timber is harvested from plantations of introduced species. These cover 1.8 million ha of land. The privatisation was limited to these forests. Indigenous forests cover 6.6 million ha – 79% of the total forest area. These were retained in public ownership and continue to be managed for amenity, conservation and environmental objectives7.

Weyerhaeuser is a global forest products company which manages over 8 million hectares of forest in North America on a sustainable basis. As regards its US holdings, it notes : “In some states, we allow public access to company land for recreational purposes when compatible with company operations. Some locations require access fees or leases. Other locations may be open during a portion of the year (such as hunting season) and some may not be open at all. Unfortunately, problems associated with illegal dumping, vandalism and damage to young seedlings have forced Weyerhaeuser to tighten restrictions regarding public access to our forests”.

Conclusions

There is a best case scenario where the harvesting rights are sold for a substantial sum to a company that does not subsequently encounter financial difficulties, brings productive innovations to forest stewardship in Ireland, encourages and facilitates public access, harvests the wood on a sustainable basis, including the protection of water systems and biodiversity. In principle, well drafted terms of reference, wise selection, well drafted and implemented agreements that are robust in the face of legal challenge, professional supervision and regulation, and good luck could deliver such outcomes. There is the worst case scenario where the purchaser encounters financial difficulties, harvests more wood than is sustainable, and/or does it in fashions that are environmentally deleterious, limits public access, and successfully challenges in court implicit or explicit agreements.

The Old Head of Kinsale Head golf course case provides an interesting insight into the relevance of property right assignment, planning and public access for recreation and amenity. This part of County Cork juts into the Atlantic, with striking views of ocean, meadow and cliffs, and a lighthouse at the end of the promontory. Although privately owned, it was widely used by the public for hiking and recreation. The land owner offered it for sale to Cork County Council for £300,000 but the offer was not accepted. He then sold it to an entrepreneur who developed it as a golf course. An Bord Pleanála attempted to impose a condition on the development which would require that the public have access, and that they could only be charged the costs of insurance and administration. In 2003, the Supreme Court found unanimously in favour of the developer, on the basis that the planning authority was exceeding its legal authority in imposing such a condition. In this case, there were a number of circumstances which may have relevance to the provision of access by Coillte and the prospective purchaser of the harvesting rights: prior to the development, although there was considerable use by the public of the Old Head, there was no public access as of right to any part of the Old Head; there was no precedent where a condition of public access was attached to a grant of planning or retention permission in respect of adjoining lands; the developer had indicated, prior to the first application for permission, a willingness to accept and facilitate a measure of public access and had not appealed conditions in that regard contained in the original planning permission; though there is statutory provision for the creation by order of the planning authority of public rights of way over lands, this had not been availed of in the present case. See the judgement here

In practise, we would likely end up somewhere between these two extremes. It is possible, and perhaps likely, that Coillte’s performance could be improved in regard to timber and environmental and amenity management. In an article in the Financial Times celebrating the Nobel Prize in Economics for 2012 (one of the awardees was Alvin Roth), Tim Harford wrote8 : “Many of the markets Professor Roth has designed do not work perfectly. A lot of theoretical economics is concerned with proving that perfection is possible. Professor Roth is interested in answering the question ‘is this good enough?” My conclusion is that the company’s performance is probably ‘good enough’ and it should be allowed to continue. However, the data underpinning performance should be improved, it would help to have some independent and publicly available assessment of commercial, amenity and environmental performance, and there is a case for allowing a new entrant to manage say 20-30 thousand hectares of mature forest to show what they can do, and what innovations and productive insights could be transferable to the management of Coillte and of the private forests as they progress to maturity. But in the Irish context, publicly owned land generally, and forest land in particular, is relatively scarce; the agenda of government should be to hold onto most of what we have created.

Notes

Declaration of Interest. Acquiring a profession involves also acquiring a set of values and prejudices which shape attitudes. When I studied forestry in UCD, we had the sense of recreating for posterity that which was lost, and the course involved a ‘practical year’ during which, inter alia, we planted trees, some of which might have been part of the harvesting sale. This immersion may influence my analysis and conclusions.

I am grateful for the feedback(including additional reference material) on an earlier draft provided by Publicpolicy.ie Board Member Mary Walsh

1. Area Planted, and Finance Data on area planted, wood prices etc. are available in: Irish Timber Growers Association, Forestry and Timber Yearbook 2013, www.forestryyearbook.ie Financial and related information on Coillte is available in the Annual Report 2011

2. Recreation Valuation Estimates on recreation valuation are derived from Mayor, Karen; Scott, Sue; Tol, Richard S. J. (2007) : Comparing the travel cost method and the contingent valuation method: An application of convergent validity theory to the recreational value of Irish forests, Working Paper, The Economic and Social Research Institute (ESRI), Dublin, No. 190 They used a 1998 survey data set compiled by UCD (Peter Clinch) and ESRI (Williams) Over 1,200 households in the electoral register were randomly selected, and surveyed. They applied two well recognised approaches to recreation valuation – contingent valuation methods (CVM) and the travel cost method (TCM) to the same data set to estimate the value per visit of the recreation experience in Irish forests. Mayor et al conclude that “The analysis shows that the CVM formulation employed does not produce a reliable estimate of Willingness to Pay (WTP) and in this case it is the value of consumer surplus from the TCM, i.e. IR£2.40 per adult equivalent per trip, that is considered the better estimate. The WTP estimate was less than half this value with about a third of responses being zero or protest bids.” Converting the IR£ value of 2.40 to Euro (X 1.27) and to 2012 Euro (inflation from 1998 to 2012 was 40.1%(Annual Average Consumer Price Index) : 2.40 X 1.27 X 1.401 = €4.27 per visit. Applying this to 18 million visits yields a value of €77 million.

3. Forestry Facts Source: Peter Bacon and Associates: Assessment of the Consequences of the Proposed Sale of Coillte’s Timber Harvesting Rights January 2013

4. Importing wood, wood products and bark – requirements for landing controlled material into Great Britain. Forestry Commission, 2007.

5. The Bacon Associates report estimates the present value of Coillte’s revenues foregone as a cost of the sale. To estimate these costs, in an analytical oddity, they use a real discount rate of 3.5 per cent, rather than using the 8 per cent rate that they used to derive the discounted value of the benefits of the sale. This asymmetry has the effect of making the net present value of costs very large relative to benefits; if the 8 per cent rate were applied, these costs would be cut in half. Given the high opportunity costs of public funds when – as in the case of Ireland – sovereign debt is such a challenge, this difference is difficult to justify.

6. This is approximately the amount the Irish carbon tax raises in two years.

7. I worked in the US, France, Germany and Switzerland. I was struck by how extensive, accessible, biologically rich, diverse and freely available publicly owned forest recreation experiences in these countries are relative to Ireland.

8. “How to find a perfect match for a Nobel”, Financial Times, Oct 20 and 21, 2012, p. 14

Annex Table 1. Some Forestry Facts

.

.

About author

79 Merrion Square, Dublin 2, Ireland

tel: 353 (1) 676 0414 | email: info@publicpolicy.ie

Company registration number: 504956

Privacy Policy | Chairman's Blog | Events | Video | Public Policy Documents | News Property Tax Ireland | Pension Reform Ireland | Water Charges Ireland