The Carbon Tax – 7 Years On

14 Jul 2016Key Point

The carbon tax has collected over €2 billion in revenue since it was introduced in Budget 2010. There is scope to increase this and use the money to reduce other taxes.

Introduction

The Carbon Tax was introduced in Budget 2010 on a phased basis. The tax applies to CO2 emissions from the non-ETS (Emissions Trading Scheme1 ) sector; mainly transport and heating.

Ireland has binding EU targets to reduce the amount of greenhouse gas (GHG) emissions produced by 20% in 2020 (relative to 2005 levels), and a target of a 16% share of renewable energy in final energy consumption. The carbon tax acts as a means of discouraging the combustion of oils, natural gas and solid fuels which contribute to GHG emissions, while also raising revenue for the exchequer.

Emissions

Ireland’s target for 2020 is to reduce GHG emissions from the non-Emissions Trading Scheme (non-ETS) sector by 20% on 2005 levels. The non-ETS sector covers emissions from agriculture, transport, residential, commercial, non-energy intensive industry and waste sectors. For all but four Member States (Luxembourg, Ireland, Belgium and Austria) projected emissions in 2020 are below the domestic targets set under the EU Effort Sharing Decision.

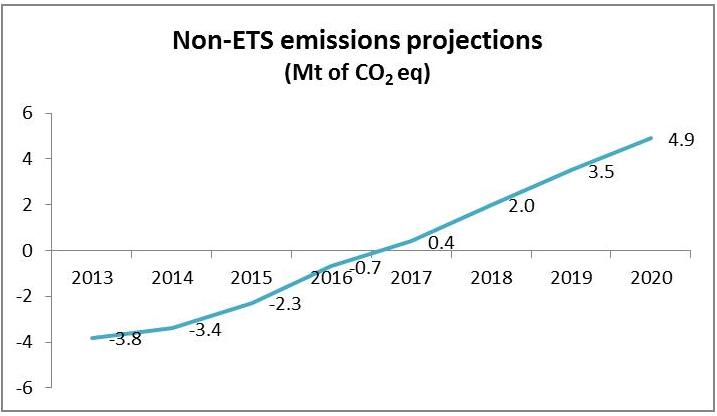

EPA projections estimate that emissions in Ireland will be 6 – 11% below 2005 levels by 2020 (9-14% off target). The European Commission expect that Ireland will exceed its emission limits each year from 2017 to 2020. Figure 1 illustrates the projections for non-ETS emissions in Ireland up to 2020 based on existing policy measures.

Figure 1

(Source: European Commission, 2015)

Ireland would exceed its binding limit by 13 per cent or 4.9 Mt of CO2 eq in 2020 based on these projections. Ireland’s provisional 2014 GHG emissions for non-ETS sectors are 42.24 Mt CO2 eq. The target for 2014 was 45.761 Mt CO2 eq. However, the EPA estimates that Ireland will breach these limits in 2016 and 2017.

Over the period 2013-2020 Ireland is projected to cumulatively exceed its compliance obligations by between 3 and 12 Mt CO2 equivalent. The cost of exceeding emissions by this amount could cost in the region of €60m to €240m (€20 per tonne of CO2 eq).

Revenue

Since its introduction, the carbon tax has raised €2.1 billion in revenue. As a percentage of income tax receipts in 2015 (€18.4bn), the carbon tax is equivalent to 2.2 per cent. Table 1 shows the figures from 2010 to 2015.

Table 1 – Carbon Tax Receipts 2010 – 2015, € millions

Price of Carbon

The original rate of €15 per tonne of CO2 was increased to €20 in 2012. The rate of €10 per tonne on solid fuel, introduced in May 2013, increased to €20 per tonne a year later. The EPA (2015)2 assumes that carbon prices for the ETS and non-ETS sectors will rise from €10 (ETS) and €20 (non-ETS) in 2020 to €35 in 2030 and €57 in 2035 respectively.

The electricity generating sector which is separately regulated by the carbon price set by the Emissions Trading Scheme (ETS) has the cap and trade scheme to provide a clear policy path towards a low carbon transition. The ETS is operated at EU level. The EU target is to reduce the emissions cap by 1.74% each year until 2020. From 2021, it is expected to reduce by 2.2% a year. In line with the reduction in the cap, the carbon price will progressively rise forcing industries in the ETS to pay an increasing price for their emissions and encouraging a switch to low-carbon alternatives.

Increasing the price of carbon by €5 would yield over €100m per annum. This would add about one per cent to the price of diesel and petrol. This revenue may be necessary to assist in paying financial penalties should the 2020 targets not be achieved.

___________________________

Notes:

1 The EU Emissions Trading Scheme (ETS) is the largest international system for trading greenhouse gas emission allowances. It covers more than 11,000 power stations and industrial plants in 31 countries, as well as airlines. The ETS operates on a ‘cap and trade’ basis.

2 EPA, (May, 2015) Ireland’s Greenhouse Gas Emissions Projections 2014-2035

{kind=link}

About author

79 Merrion Square, Dublin 2, Ireland

tel: 353 (1) 676 0414 | email: info@publicpolicy.ie

Company registration number: 504956

Privacy Policy | Chairman's Blog | Events | Video | Public Policy Documents | News Property Tax Ireland | Pension Reform Ireland | Water Charges Ireland